Key Takeaways

- Market Disconnect Persists: Uranium spot prices have held up and long-term prices have strengthened, but uranium mining equities have lagged as investor sentiment remains cautious.

- Long-Term Pricing Sends a Stronger Signal: The long-term uranium price reached its highest level in 18 years, pointing to tighter utility procurement conditions and higher incentive pricing for new supply.

- Energy Security is Reshaping Demand: Geopolitical risk, AI-driven electricity demand, industrial reshoring and grid reliability concerns are strengthening the case for nuclear power.

- Policy Support Is Turning into Execution: The U.S., Canada and Europe are moving from broad nuclear ambitions toward financing, regulatory reform, life extensions, restarts and fuel-cycle investment.

- Uranium Supply Remains Constrained: Utilities remain under-contracted, secondary inventories are dwindling and new uranium production faces long permitting timelines, high capital needs and development risk.

- Uranium’s Setup Continues to Improve: Despite short-term market weakness, the sector remains supported by a durable imbalance between strategic demand and slow-to-respond supply.

Performance as of June 30, 2026

| Metric | 1 MO* | 3 MO* | YTD* | 1 YR | 3 YR | 5 YR |

| U3O8 Uranium Spot Price1 | 0.10% | 1.08% | 4.28% | 8.24% | 14.93% | 21.42% |

| Uranium Mining Equities (VettaFi Global Uranium Mining Index)2 |

-14.40% | -15.15% | -3.91% | 14.92% | 20.89% | 15.39% |

| Uranium Junior Mining Equities (Nasdaq Sprott Junior Uranium Miners Index TR) 3 |

-17.46% | -18.07% | -7.43% | 19.76% | 17.48% | 10.13% |

| Broad Commodities (BCOM Index)4 | -8.83% | -8.92% | 12.30% | 20.74% | 6.67% | 5.43% |

| U.S. Equities (S&P 500 TR Index)5 | -0.95% | 15.20% | 10.21% | 22.32% | 20.59% | 13.40% |

*Performance for periods under one year is not annualized.

Source: Bloomberg as of 6/30/2026. You cannot invest directly in an index. Past performance is no guarantee of future results.

Performance Overview: Fundamentals Lead, Market Lags

Uranium entered mid-year with a stronger fundamental backdrop than market performance would suggest, as rising long-term prices, improving policy support, growing electricity demand and constrained supply continued to reinforce the investment case despite disappointing short-term returns across uranium mining equities.

The first half of the year was characterized by a widening, and somewhat frustrating, disconnect between uranium market fundamentals and price performance. In June, the uranium spot price remained relatively flat, rising 0.10%, while the long-term price advanced to its strongest level in this cycle. Uranium mining equities, however, declined 14.40%, and junior uranium miners fell 17.46%. Year to date, spot uranium is up 4.28%, while uranium miners are down 3.91% and junior uranium miners are off 7.43%. That performance has been frustrating, particularly because the underlying uranium setup has improved through the first half of the year.

Uranium fundamentals are strengthening beneath the surface, even as equities lag.

In our view, this performance divergence reflects a combination of near-term market uncertainty, risk-off positioning and subdued investor sentiment rather than any deterioration in the sector's underlying fundamentals. For much of this year, investor attention has been largely focused on AI (artificial intelligence), geopolitical tensions in the Middle East, energy security and broader macroeconomic uncertainty. Ironically, these same themes have reinforced the long-term investment case for uranium. The rapid expansion of AI data centers, reshoring, advanced manufacturing and electrification are accelerating the demand for reliable, base load electricity. The U.S.-Iran conflict and concerns over the security of critical hydrocarbon transit routes have reinforced the strategic importance of energy security. Nuclear power has the potential to provide a solution, offering large-scale, reliable, 24/7 generation with fuel requirements less susceptible to supply shocks.

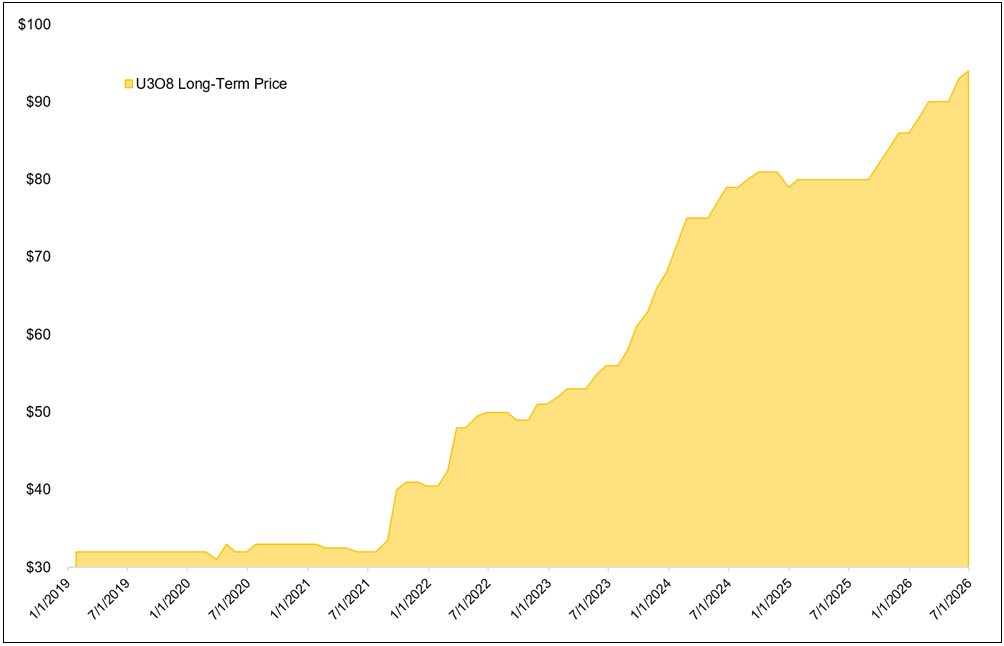

The term market continues to provide the clearest signal of the uranium market's underlying strength. While the spot price has moderated since briefly exceeding $100/lb earlier this year, the long-term uranium price has continued to advance, reaching $94/lb at the end of June (see Figure 1), its highest level in 18 years. This matters because the long-term market is more closely tied to utility procurement, project economics and the incentive pricing required to bring new supply online. A rising long-term price shows that the market remains tight, even if equity markets don’t reflect it.

Figure 1. U308 Long-Term Price Continues to Strengthen to New Cycle Highs (2019-2026)

Source: Bloomberg and UxC. Data as of 6/30/2026. U3O8 Long-Term Price is measured by the UxC Uranium U3O8 Long-Term Price (UXCPULTM UXCP Index). You cannot invest directly in an index. Past performance is no guarantee of future results.

Policy Momentum Meets Supply Constraints

Major announcements continue to highlight the renewed focus on nuclear energy. The U.S. Department of Energy announced $17.5 billion in conditional loans to fund long lead time items for up to 10 new reactors. Canada also released a Nuclear Energy Strategy focused on new builds, reactor exports, uranium production and fuel-cycle opportunities. Urenco USA announced a multi-billion-dollar expansion of the only commercial-scale uranium enrichment facility in the U.S. Belgium and Italy have reconsidered nuclear’s role after years of phase-out politics. These developments show that nuclear support is increasingly shifting from policy language to financing, licensing, fuel-cycle investment and practical execution.

Nuclear momentum is accelerating, but uranium supply cannot keep pace.

The supply of uranium could become a limiting factor without contractual commitments by utilities to support additional production. Utilities have under-contracted for more than a decade, and the resulting gap has been partly filled by secondary inventories that have been dwindling. The forecasted uncovered uranium requirements curve now exceeds 3 billion pounds through 2045, necessitating a doubling of primary uranium production. Higher uranium prices have helped restart projects and improve producer economics, but uranium supply cannot respond quickly. Large deposits are difficult to find, permitting remains complex and many projects require years of development before they can meaningfully contribute to production.

In our view, these positive developments suggest that the recent underperformance of uranium mining equities may prove to be more of an opportunity than a warning signal. The market has marked down uranium miners and juniors during a period when the long-term price has advanced, nuclear policy has strengthened, fuel-cycle security has become more strategic and the supply response remains constrained. We believe that uranium miners are well supported by a growing imbalance between strategic demand and uncertain future supply. If utility contracting accelerates in the second half of the year, the current gap between market performance and fundamentals could begin to close.

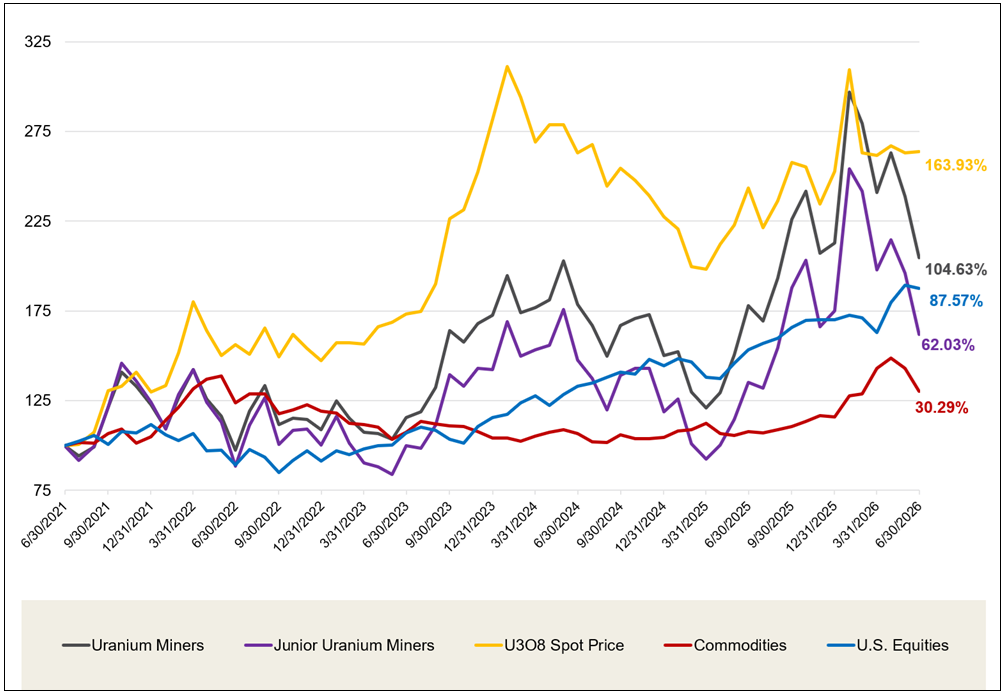

Looking at longer-term performance, uranium and uranium miners have meaningfully outpaced equities and broader commodity benchmarks over the past five years (see Figure 2).

Figure 2. Physical Uranium and Uranium Stocks Have Outperformed Other Asset Classes Over the Past Five Years (6/30/2021-6/30/2026)

Source: Bloomberg and Sprott Asset Management. Data as of 06/30/2026. Uranium Miners are measured by the Northshore Global Uranium Mining Index (URNMX index); Junior Uranium Miners are measured by the Nasdaq Sprott Junior Uranium Miners™ Index (NSURNJT™ Index); U.S. Equities are measured by the S&P 500 TR Index; the U308 Spot Price is from TradeTech; and Commodities are measured by the Bloomberg Commodity Index (BCOM). Definitions of the indices are provided in the footnotes. Past performance is no guarantee of future results.

Sprottlight: Energy Security Strengthens Nuclear’s Role

Middle East Risk Has Repriced the Value of Energy Security

Energy security has emerged as a strategic priority. Middle East tensions and growing concerns over critical oil and gas transit routes have exposed the fragility of global energy supply chains. Despite ongoing efforts to diversify energy sources, the world's continued reliance on hydrocarbons leaves economies vulnerable to geopolitical shocks, supply disruptions and volatile energy prices.

Nuclear power offers a fundamentally different energy-security model. Uranium is highly energy dense, reactor fuel can be planned and stored well in advance, and nuclear plants can operate continuously once fuel is loaded. While this does not fully eliminate nuclear supply-chain risk, it does make nuclear power less exposed to the short-term volatility that can affect hydrocarbon markets. In an environment where governments are reassessing energy dependence, nuclear power’s resilience is becoming more valuable.

Nuclear power has moved beyond the energy transition narrative and has become a strategic pillar of energy security.

Nuclear's growth is no longer driven primarily by decarbonization. It is increasingly a response to energy security. The Russia-Ukraine war and recent disruptions around the Strait of Hormuz have exposed the vulnerability of fossil fuel supply chains to geopolitical conflict, maritime chokepoints and trade disruptions. At the same time, AI data centers, electrification, advanced manufacturing and industrial reshoring are driving a sharp increase in demand for reliable, around-the-clock electricity. Nuclear power addresses both challenges by providing carbon-free baseload generation powered by fuel that can be secured years in advance. As a result, uranium is becoming a strategic resource, not only for the energy transition, but also for energy security, grid reliability and economic competitiveness.

China provides the clearest example of this shift. While China leads the world in renewable energy deployment, its clean energy expansion is fundamentally an energy security strategy. As one of the world's largest energy importers, China has long sought to reduce its dependence on imported fossil fuels, volatile commodity markets and vulnerable maritime trade routes. Its unprecedented investment in renewable power, transmission infrastructure, energy storage and nuclear generation reflects a deliberate effort to build a more secure, self-reliant and resilient electricity system capable of supporting industrial growth, electrification and AI-driven power demand.

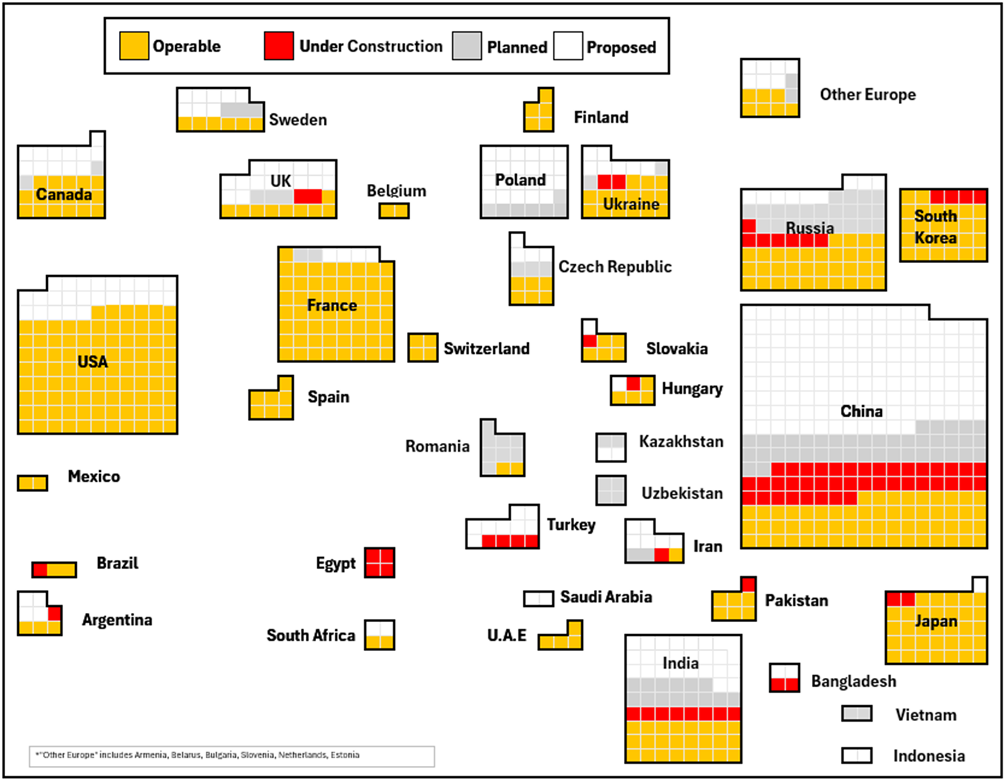

Nuclear power sits at the center of that strategy. China accounts for 38 of the 79 reactors currently under construction worldwide and 41 of the 121 reactors in the global development pipeline (see Figure 3). This sustained pace of construction demonstrates that China's nuclear expansion is not a cyclical investment program, but a decades-long strategic commitment to energy independence.

The implications for uranium are profound. Recognizing the strategic importance of nuclear fuel, China has secured long-term uranium supply through offtake agreements, strategic inventories and investments in upstream mining assets. By contrast, many Western utilities remain under-contracted, secondary supply continues to decline and new mine development remains constrained by lengthy permitting timelines and capital requirements.

The same strategic logic is increasingly taking hold across the West. Governments are moving beyond broad policy support and toward concrete implementation through financing programs, regulatory reform, reactor life extensions, restarts and new-build commitments. This matters because uranium demand ultimately depends on reactors being built, restarted and kept in operation. As nuclear policy transitions from aspiration to execution, the long-term fundamentals supporting uranium remain strong.

Figure 3. World’s Nuclear Buildout

Source: World Nuclear Association as of 07/06/2026.

Canada: A Strategic Nuclear Supply Chain Takes Shape

Canada is positioning itself as a global nuclear leader with the launch of its Nuclear Energy Strategy in June 2026.6 The plan supports up to 10 new large-scale reactors through federal financing, tax incentives and faster approvals, helping unlock investment in capital-intensive nuclear projects. The Strategy extends beyond reactor deployment, targeting a larger role for Canada in the global uranium market and aiming to double exports by 2035 as new production ramps up.

Canada is positioning itself as a cornerstone of the Western nuclear renaissance.

The Strategy’s fuel-cycle focus is particularly significant, as it recognizes that geopolitical fragmentation has exposed vulnerabilities across nuclear supply chains, from mining and milling to conversion, enrichment and fuel fabrication. As Western and allied countries seek to reduce exposure to Russian nuclear fuel services, secure and reliable alternative suppliers are becoming increasingly strategic.

Canada is already well positioned in the upstream market as the world’s second-largest uranium producer, with the world’s largest high-grade uranium deposits concentrated in Saskatchewan’s Athabasca Basin. The Strategy also creates a pathway for selective downstream expansion, strengthening Canada’s role in secure nuclear fuel supply chains for Canada and its allies.

Canada is not only pursuing long-term nuclear ambitions; 2026 is also a pivotal year for nuclear construction. Ontario is advancing the first Small Modular Reactor (SMR) project in the G7 at the Darlington New Nuclear Project.7 In April 2026, Ontario announced the installation of a 2.1-million-pound basemat module for Unit 1, marking the first foundation of a new nuclear reactor built in Ontario in more than three decades. The first SMR unit is expected to generate enough electricity to power approximately 300,000 homes, while all four planned units are expected to supply power for roughly 1.2 million homes.

SMRs broaden the potential pathways for nuclear deployment. Smaller than traditional large reactors, they are designed around standardized, repeatable construction approaches that may make them better suited for certain grids, industrial applications and jurisdictions that require reliable baseload power without the scale and complexity of a conventional reactor project.

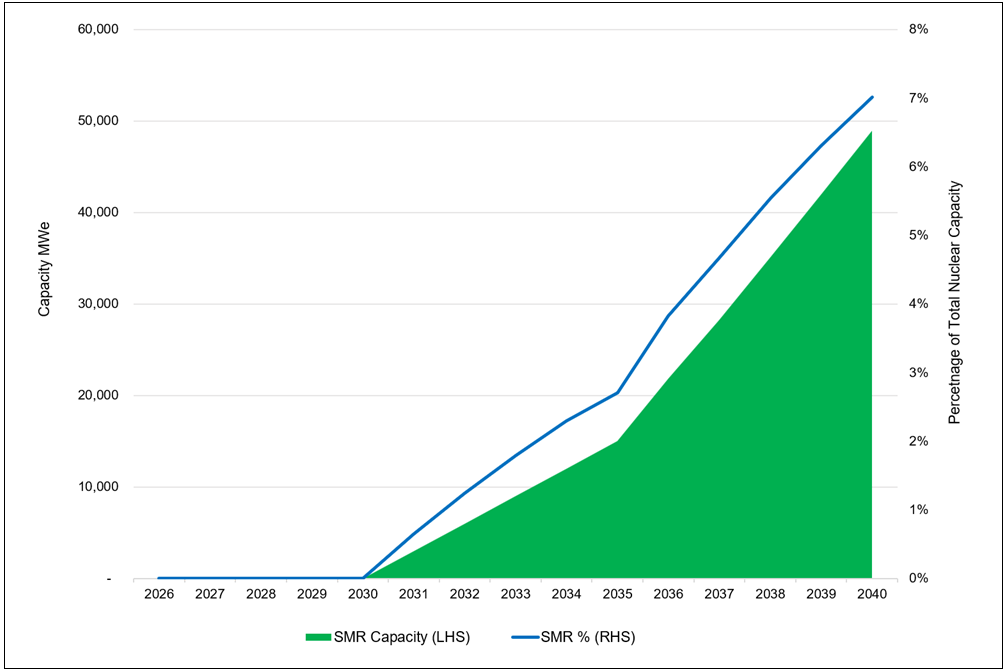

The outlook for SMRs is also improving. The World Nuclear Association’s latest fuel outlook increased its forecast for SMR capacity in 2040 by 42% from the prior estimate, with SMRs now expected to account for 7% of global nuclear generation by 2040 (see Figure 4). While still a modest share of total nuclear output, the trajectory highlights growing interest in SMRs as governments and industries seek reliable, scalable and secure electricity solutions.

Ultimately, Canada’s policy direction is increasingly supportive of both uranium supply and nuclear demand. By advancing new reactor construction, uranium export growth, fuel-cycle capabilities and next-generation nuclear technologies, Canada is positioning itself as a critical contributor to the secure energy systems being developed by Western economies.

Figure 4. World’s SMR Buildout

Source: WNA, World Nuclear Fuel Report: Global Scenarios for Demand and Supply Availability 2025-2040.

U.S. Nuclear Policy Moves Toward Execution

In June 2026, the U.S. Department of Energy (DOE) announced a $17.5 billion conditional loan commitment to accelerate the deployment of up to 10 large-scale nuclear reactors by as much as three years.8 Each reactor is expected to generate 1.1 GW of power, with the combined output of all 10 units capable of supplying electricity to nearly 10 million U.S. households.

The nuclear revival is also extending beyond new construction, with renewed efforts to bring previously stalled assets back online. In June 2026, Santee Cooper advanced plans to restart the V.C. Summer nuclear project in South Carolina.9 While the project remains subject to further evaluation, the move reflects a broader U.S. push to preserve and expand existing nuclear capacity. Similar restart efforts are underway at Palisades in Michigan and Three Mile Island Unit 1 in Pennsylvania, as rising electricity demand increases the strategic value of reliable, always-on power.

America’s nuclear revival is moving from policy to projects.

Life extensions are equally important because the fastest source of nuclear demand is often the reactor already operating. In April 2026, the Nuclear Regulatory Commission (NRC) approved a 20-year extension for California’s last nuclear power plant, allowing Diablo Canyon Units 1 and 2 to operate into the mid-2040s.10 Extending the life of existing reactors preserves reliable baseload generation and sustains uranium demand without waiting years for new capacity to come online.

Regulatory reform is the foundation supporting this broader nuclear expansion. In March and April 2026, the NRC outlined clearer licensing pathways and an 18-month review target for new and advanced reactor projects.11 These efforts build on the May 2025 executive orders focused on rebuilding the U.S. nuclear industrial base, reforming the NRC and linking nuclear deployment to energy security, AI-driven electricity demand, national security and fuel-cycle resilience. The administration’s broader goal is to quadruple U.S. nuclear capacity from roughly 100 GW to 400 GW by 2050, while regulatory reforms aim to speed up and make approvals more predictable. Together, these measures increase the likelihood that policy commitments translate into actual uranium demand.

The nuclear fuel cycle is also becoming a strategic priority. In June 2026, Urenco USA announced a multi-billion-dollar expansion of the country’s only commercial-scale uranium enrichment facility, adding 2.1 million SWU of capacity and increasing output by nearly 50%. The investment reflects growing Western efforts to reduce reliance on Russian enrichment services following the invasion of Ukraine and rebuild a more secure nuclear fuel supply chain.

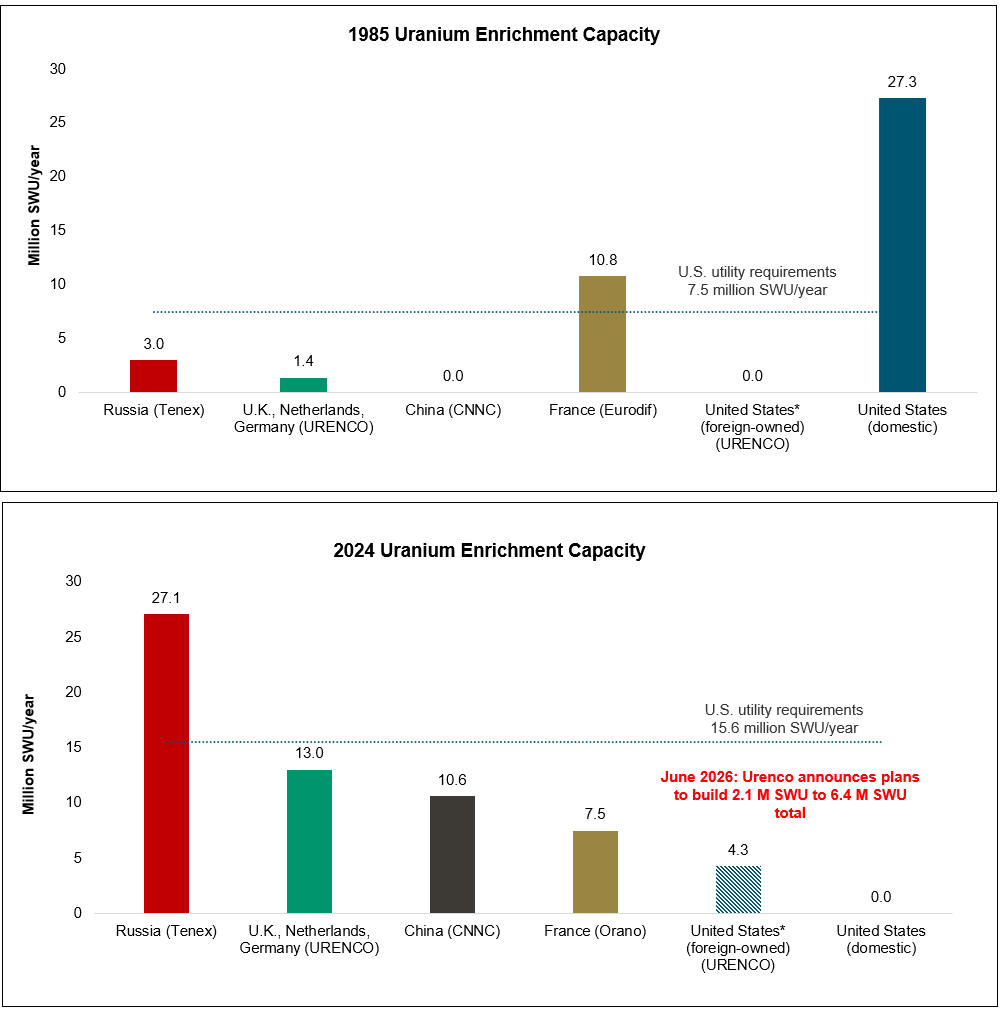

The challenge is significant. The U.S. has fallen from global leadership in uranium enrichment to having limited domestic fuel-cycle capacity, while uranium mining production has declined sharply (see Figure 5). Rebuilding the full nuclear supply chain—from mining and conversion to enrichment and fuel fabrication—has become a strategic priority as nuclear demand accelerates.

Taken together, U.S. policy is creating a more supportive environment for uranium markets. New reactor financing, project restarts, life extensions, enrichment investment and regulatory reform are all advancing the same objective: converting nuclear ambition into operating capacity and secure fuel supply. For uranium, this strengthens the long-term demand outlook while highlighting the importance of reliable, diversified supply.

Figure 5. The Loss of U.S. Nuclear Fuel Leadership: 1985 vs. 2024 Uranium Enrichment Capacity

Source: 2024 data from World Nuclear Association Nuclear Fuel Report 2025. 1985 data from the Congressional Budget Office. Centrus Energy Corp. Urenco.

*The only remaining enrichment plant physically located in the U.S. is controlled by URENCO, a European-owned corporation.

Looking Ahead: Uranium’s Setup Continues to Strengthen

For uranium investors, the message is clear: nuclear policy is moving from reassessment to execution. As governments prioritize energy security, grid reliability and fuel-cycle resilience, uranium demand appears increasingly well supported through the remainder of the decade.

The uranium market is shifting from policy-driven optimism to fundamentals-driven scarcity.

Contracting remains an important catalyst for the uranium market. Utilities have under-contracted for 13 consecutive years, leaving 2026 term volumes well below the replacement rate and creating accumulated procurement needs that still must be addressed. At the same time, Western inventories appear strategically low, secondary supplies are less able to bridge the gap between mine production and reactor demand, and producers are increasingly reluctant to commit future supply at prices that do not reflect scarcity, development risk and rising replacement costs.

Policy support should remain a major market driver in the second half of the year and beyond as nuclear policy shifts from ambition to implementation. Recent developments in the U.S., Canada and Europe point in the same direction: reactor financing, restarts, life extensions, regulatory reform, fuel-cycle investment, uranium export growth and renewed interest in nuclear as a source of energy security, grid reliability and industrial resilience.

Supply remains the limiting factor. Higher uranium prices have supported restarts, project development and stronger producer economics, but uranium supply cannot respond quickly. Large deposits are difficult to find, permitting remains complex, project timelines are long and many new mines require sustained long-term prices before capital can be committed. Production shortfalls, operational interruptions, permitting delays or geopolitical disruptions could tighten the market more quickly than expected, particularly when utilities remain under-contracted and new supply is slow to develop.

We believe the mid-year outlook remains structurally bullish. Uranium has consolidated after a strong start to the year, but the market’s foundations have continued to improve. Nuclear power is increasingly aligned with the issues investors are already focused on: electricity scarcity, energy security, AI-driven power demand and fuel-cycle resilience. If utility contracting accelerates in the second half of the year, the market may begin to price the imbalance between strategic demand and constrained supply more directly.

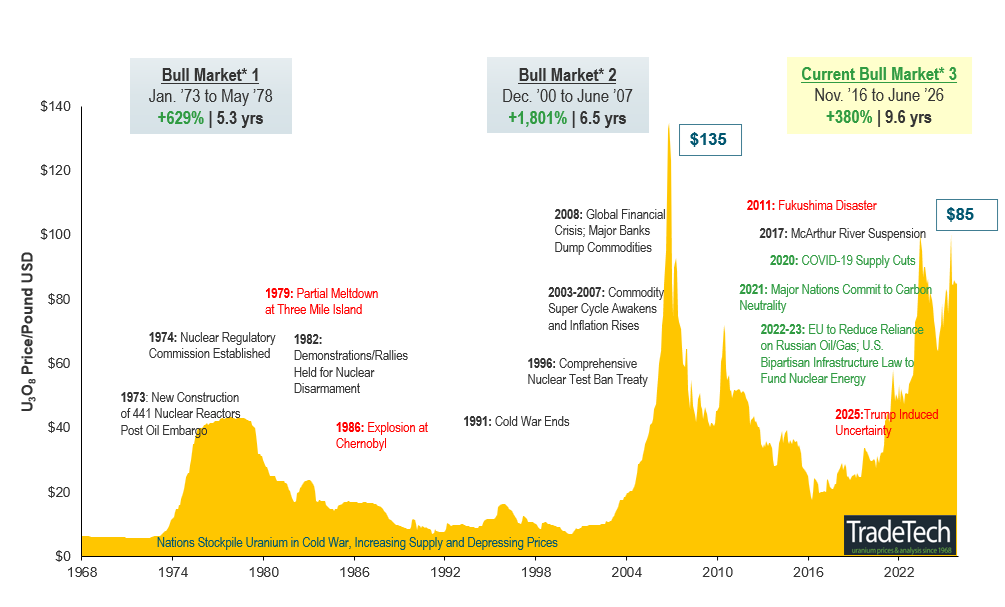

Figure 6. Uranium Bull Market Is Still Intact on Long-Term Fundamentals (1968-2026)

View Larger PDF Version of this Chart

Note: A “bull market” refers to a condition of financial markets where prices are generally rising. A “bear market” refers to a condition of financial markets where prices are generally falling.

Source: TradeTech Data as of 6/30/2026. TradeTech is the leading independent provider of uranium prices and nuclear fuel market information. The uranium prices in this chart, dating back to 1968, are sourced exclusively from TradeTech; visit https://www.uranium.info/

Footnotes

| 1 | The U3O8 uranium spot price is measured by a proprietary composite of U3O8 spot prices from UxC, S&P Platts and Numerco. For periods before July 2021 data is from TradeTech LLC. |

| 2 | The VettaFi Global Uranium Mining Index (URNMX) was created by North Shore Indices, Inc. (the “Index Provider”). The index was acquired by VettaFi, a differentiated index provider with modern distribution solutions and a subsidiary of TMX Group, and as of 4/30/2026 it was renamed the VettaFi Global Uranium Mining Index. VettaFi is responsible for the ongoing maintenance of the Index. The Index is calculated by VettaFi, which is not affiliated with the North Shore Global Uranium Miners Fund (“Existing Fund”), ALPS Advisors, Inc. (the “Sub-Adviser”) or Sprott Asset Management LP (the “Adviser”). |

| 3 | The Nasdaq Sprott Junior Uranium Miners™ Index (NSURNJ) is designed to track the performance of mid-, small- and micro-cap companies in uranium-mining related businesses. |

| 4 | The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index that tracks prices of futures contracts on physical commodities and is designed to minimize concentration in any one commodity or sector. It currently has 23 commodity futures in six sectors. |

| 5 | The S&P 500 or Standard & Poor's 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. |

| 6 | Source: Government of Canada. Nuclear Energy Strategy for Canada. |

| 7 | Source: Ontario Completes Major Milestone on G7’s First Small Modular Reactor. 4/30/2026. |

| 8 | Source: The U.S. Department of Energy, Department of Energy Announces American Nuclear Supply Chain Loans, 6/23/2026 |

| 9 | Source: TheState.com, Santee Cooper steams ahead with plans to restart V.C. Summer nuclear project, 6/29/2026. |

| 10 | Source: Reuters, US regulators grant California's last nuclear power plant 20-year operating life extension, 4/3/2026. |

| 11 | Source: Reuters, NRC rolls out reforms to accelerate small reactor licensing, 5/26/2026. |

| 12 | Source: Urenco.com, Urenco USA Plans Significant Expansion of U.S. Uranium Enrichment Capacity, 6/2/2026. |

Investment Risks and Important Disclosure

Relative to other sectors, precious metals and natural resources investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Gold and precious metals are referred to with terms of art like "store of value," "safe haven" and "safe asset." These terms should not be construed to guarantee any form of investment safety. While “safe” assets like gold, Treasuries, money market funds and cash generally do not carry a high risk of loss relative to other asset classes, any asset may lose value, which may involve the complete loss of invested principal.

Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary and opinions are unique and may not be reflective of any other Sprott entity or affiliate. Forward-looking language should not be construed as predictive. While third-party sources are believed to be reliable, Sprott makes no guarantee as to their accuracy or timeliness. This information does not constitute an offer or solicitation and may not be relied upon or considered to be the rendering of tax, legal, accounting or professional advice.