Key Takeaways

- Uranium markets posted varied performance in March, with the U3O8 uranium spot price declining 6.84%, from US$94.60 to $88.13 per pound. By contrast, uranium miners and junior uranium miners rose, gaining 1.75% and 2.52%, respectively.

- One key factor influencing market behavior is the strategic positioning of buyers, who appear to be abstaining from active participation in the market.

- Over the longer term, physical uranium and uranium miners have demonstrated significant outperformance against broad asset classes, particularly other commodities.

- Given the increasing global recognition of nuclear energy's importance to energy security and decarbonization, the demand for uranium is forecasted at 338 million pounds in 2040, requiring the supply to double by then.

- Kazatomprom, the world’s largest uranium producer, cannot increase production in 2024 despite the U3O8 spot price increasing to well over their mines' incentive levels.

Performance as of March 31, 2024: Average Annual Total Returns

| Asset | 1 MO* | 3 MO* | YTD* | 1 YR | 3 YR | 5 YR |

|

U3O8 Uranium Spot Price 1 |

-6.84% | -3.26% | -3.26% | 73.83% | 40.68% | 28.43% |

|

Uranium Mining Equities (Northshore Global Uranium Mining Index) 2 |

1.75% | 2.56% | 2.56% | 64.97% | 26.33% | 30.24% |

| Uranium Junior Mining Equities (Nasdaq Sprott Junior Uranium Miners Index TR) 3 | 2.52% | 7.92% | 7.92% | 69.99% | 21.19% | 28.91% |

|

Broad Commodities (BCOM Index) 4 |

2.89% | 0.85% | 0.85% | -5.70% | 6.05% | 4.17% |

|

U.S. Equities (S&P 500 TR Index) 5 |

3.22% | 10.56% | 10.56% | 29.88% | 11.52% | 15.04% |

*Performance for periods under one year are not annualized.

Sources: Bloomberg and Sprott Asset Management LP. Data as of 3/31/2024. You cannot invest directly in an index. Included for illustrative purposes only. Past performance is no guarantee of future results.

Uranium's Retracement and Recovery

Uranium markets posted varied performance in March, with the U3O8 uranium spot price declining 6.84%, from US$94.60 to $88.13 per pound.1 By contrast, uranium miners and junior uranium miners rose, gaining 1.75% and 2.52%, respectively.2,3 The recent trading behavior of the uranium spot price suggests a potential bottoming in the market. In the first half of March, we witnessed a descent in the spot price, reaching a low of $83.78 before commencing a recovery that culminated at $88.13 per pound by month-end.

One key factor influencing the spot market has been a ”buyer's strike”, as some utilities and select producers have stepped away as the price broke above $100 per pound. Nuclear utilities have significantly different procurement strategies than others, such as natural gas plants. The latter needs to buy fuel consistently, but the former generally has several years of inventories. Uranium inventories within reactor cores and in various stages of the fuel cycle allow utilities to step away from the market if they are reluctant to chase a rising price.

The recent pullback in prices follows a remarkable surge that saw the uranium spot price climb by nearly 80% over seven months, from July 2023 to January 2024. February's peak of $107 marked a historic recent high before a period of profit-taking tempered the bullish momentum. However, this retreat should be viewed as a natural correction within the broader context of a bullish market cycle rather than indicative of fundamental weakness.

Despite a temporary dip to $84 mid-month, the subsequent partial rebound in price signals renewed buyer activity. Volatility is natural in the uranium markets, and gains may typically follow a staircase pattern that may provide investors with reasonable entry points—especially given that the underlying fundamentals remain strong.

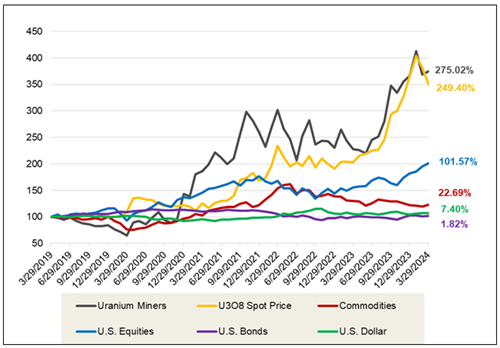

Over the longer term, physical uranium and uranium miners have demonstrated significant outperformance against broad asset classes, particularly other commodities. For the five years ended March 31, 2024, the U3O8 spot price has risen a cumulative 249.40% compared to 22.69% for the broader commodities index (BCOM), as shown in Figure 1.

Figure 1. Physical Uranium and Uranium Stocks Have Outperformed Other Asset Classes Over the Past Five Years (03/31/2019-03/31/2024)

Source: Bloomberg and Sprott Asset Management. Data as of 03/31/2024. Uranium Miners are measured by the Northshore Global Uranium Mining Index (URNMX index); U.S. Equities are measured by the S&P 500 TR Index; the U308 Spot Price is from TradeTech; U.S. Bonds are measured by the Bloomberg Barclays US Aggregate Bond Index (LBUSTRUU); Commodities are measured by the Bloomberg Commodity Index (BCOM); and the U.S. Dollar is measured by DXY Curncy Index. Definitions of the indices are provided in the footnotes. You cannot invest directly in an index. Included for illustrative purposes only. Past performance is no guarantee of future results.

Kazatomprom’s Supply Constraints Remain

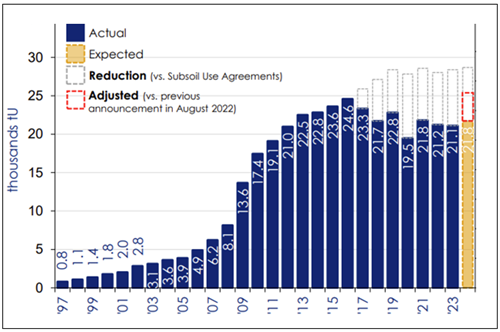

The recent retracement of the uranium spot price has not been due to weakening fundamentals. Mine supply, with a 2024 forecasted production of 156 million pounds, is still well short of the world’s uranium reactor requirements, with 176 million pounds forecasted for 2024. Further, given the increasing global recognition of the importance of nuclear energy to energy security and decarbonization, the demand for uranium is forecasted at 338 million pounds in 2040.6 To meet these 2040 projections, the uranium mine supply needs to more than double by then, but the supply response thus far has proven to be more challenging to ramp up than anticipated. In March, NAC Kazatomprom JSC (Kazatomprom) released its 2023 full-year results and reaffirmed that it would not meet its previously announced production increases for 2024 (see Figure 2). Further, the company noted that production guidance for 2025 will not be given until August.

With the significant increase in the uranium price since 2021, one would expect the world’s largest and lowest-cost producer would be well positioned and incentivized to increase production to capture the market opportunity.

Figure 2. Kazakhstan Production Volume (100% basis, per subsoil agreements)

Source: OFR reports, CPR report 2022. Production guidance for 2024 is illustrated on the chart as being in the middle of the guidance range disclosed in TU 4Q23. Adjustment refers to the difference between initial expectations for 2024 production, announced on August 19, 2022, and operating guidance, announced on February 1, 2024. Included for illustrative purposes only.

The timeline for Kazakhstan's production increases largely hinges on two things: the availability of sulfuric acid and Kazatomprom’s growth strategy. In our view, Kazakhstan benefits as a low-cost producer due to its reliance on in-situ recovery (ISR) mining methods, in contrast to Cameco's Cigar Lake and McArthur River underground mining operations. ISR mining, however, requires significant quantities of sulfuric acid, a resource of which 60% is allocated for producing fertilizers, crucial for global food supplies. The prioritization of sulfuric acid for agricultural needs may delay the pace of Kazakhstan's production ramp-up. To this end, Kazatomprom signed an agreement in January with an Italian company to construct a sulfuric acid plant in Kazakhstan to be completed in 2027. This would significantly increase the company's in-house production capacity by 800,000 tpa for a total of 1.48 million metric tons (relative to Kazatomprom’s 2023 needs of 1.7 million metric tons).7

Kazatomprom’s growth strategy will also play a pivotal role in its future supply response. For the past few years, the company has adopted a value-over-volume philosophy. The supply discipline is achieved by prioritizing the increase in the price of products/services instead of volume growth. Irrespective of the sulfuric acid shortage, Kazatomprom has recently stated it will remain committed to its "value over volume” strategy.

In the interim, we believe inventories will continue to play an important but diminishing role in balancing the market. Regarding Kazatomprom, on a 100% basis, they announced inventories of 7,242 tU. Though this would be sufficient to cover 34% of last year’s production volume (2024 will be similar in production), it also represents a 23% drop year over year.

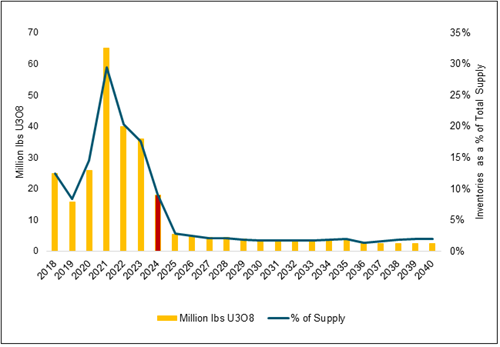

This trend is also reflective of broader commercial inventories, which are predominantly utilities. With mine supply insufficient to meet world reactor requirements, countries have been forced to rely on secondary supplies, predominantly commercial inventories. We believe that in 2024 the available-for-sale inventories have been largely depleted and that the security of supply has become paramount, which will likely lead to the rebuilding of utility uranium inventories. Figure 3 exhibits these forecast trends, with supply from commercial inventories peaking in 2021 at 65 million pounds of U3O8 (29% of total supply), falling to 18 million pounds by 2024 (9%) and diminishing thereafter.

Figure 3. Commercial Inventories Supply

Source: UxC, Uranium Market Outlook Q1 2024. Included for illustrative purposes only.

Junior Uranium Miners Advance

Fueled by rising uranium spot prices and a vast market deficit, several junior uranium mining companies are answering the industry’s call. Although small individually and collectively, these uranium mining restarts and new builds help incrementally edge supply closer to demand.

In March, Ur-Energy Inc. (Ur-Energy) announced the decision to build out its Shirley Basin Project.8 Located in Wyoming, the project is fully permitted and licensed, with a capacity to produce up to a million pounds of U3O8 per year. The project was pioneered in the 1960s, suspended operations in the 1990s due to low uranium pricing and is targeted to be in production by 2026.9 This restart follows a flurry of other miners working toward production, such as enCore Energy Corp.’s restarted Rosita Plant, which announced its first shipment of uranium in March.10

Regarding new builds, news came out from Global Atomic Corporation’s (Global Atomic) Dasa Project in the form of a positive project feasibility study. The study extended the Dasa Mine Life from 12 to 23 years, increased mineral reserves by 50% to 73 million pounds of U3O8 and increased projected uranium production from Dada by 55% to 68.1 million pounds.11 These results were well received by investors and helped support the company’s stock, which had been hurt by geopolitical considerations due to its location in Niger.

The geopolitical situation in Niger has intensified in March. For context, a military junta led a coup d'état in July 2023, overthrowing the democratically elected president. Before this, Niger had been an ally of the West, namely the U.S. However, in March, the ruling junta announced an end to a military relationship with the U.S.12 The increasingly anti-Western stance, which follows French troops leaving Niger when the two countries' military cooperation ended in December, is increasing geopolitical risk to uranium miners Orano, Global Atomic and GoviEx Uranium Inc.13 Not all risk was elevated for Nigerien operations, as the tensions had recently eased somewhat locally in West Africa. The Economic Community of West African States (ECOWAS) recently decided to lift sanctions on Niger. Regarding uranium mining, this was beneficial due to the lifting of border closures. Though the current state remains in flux, this may help ease logistical constraints. Specifically, Orano had announced significant difficulties in exporting uranium and importing necessary reagents for uranium processing.

Impactful Industry Developments

The first-ever nuclear power plant restart in the U.S. is now in sight. The U.S. Department of Energy’s Loan Programs Office announced a conditional commitment for up to a $1.52 billion loan to Holtec Palisades LLC (Holtec) to finance the recommissioning of the Palisades Power Plant.14 The 800-megawatt (MW) single-reactor nuclear power plant was retired in May 2022, and if realized, its restart would mark a notable shift in government policy toward revitalizing nuclear energy projects. Further, Holtec aims to use the site for two small modular reactor (SMR) units for an additional 800 MW of generation capacity. However, this was not part of the $1.52 billion loan. Notably, as opposed to new reactors, reactor restarts such as these and reactor extensions of life represent a more immediate source of demand. The project aims to be in commercial operation by the end of 2025 and, therefore, needs to secure the prerequisite fuel beforehand.

Orano was reported in March to be considering building an enrichment facility in the U.S.15 This continues the increasing Western efforts to reshore or friendshore uranium enrichment services. Last October, Orano decided to increase production capacity at its uranium enrichment facility in France. Further, in March, U.S. President Joe Biden signed a bill approving $2.7 billion in funding in a push for domestic enrichment capabilities.16

Russia is the largest uranium enricher, and according to Orano, the country provides about 30% of the West’s enriched uranium. The West is moving away from Russian services, given the U.S. House’s passing of the Prohibiting Russian Uranium Imports Act, which specifically prohibits the imports of Russian enriched uranium subject to certain waivers, with all imports banned by 2027. The Act remains stalled in the Senate but may provide another tailwind to the market when passed, especially given that Tenex, a Russian state-owned uranium company, has warned American customers that if this Act passes, Russia might preemptively bar exports of its supply to the U.S., further exacerbating supply uncertainty.17

Potentially Attractive Entry Point

We believe uranium's recent pause may be an attractive entry point in the overall uranium bull market. A longstanding primary supply deficit and renewed interest in nuclear energy highlight the real challenges to bring the market back into balance. With no meaningful new supply on the horizon for three to five years, we believe this bull market has further room to run. While last year’s multiyear record in long-term uranium contracting was celebrated, the overall numbers disguise a bifurcated market. Some utilities are well covered, while others have ignored the powerful market signals and adapted their procurement strategies to the new market realities.

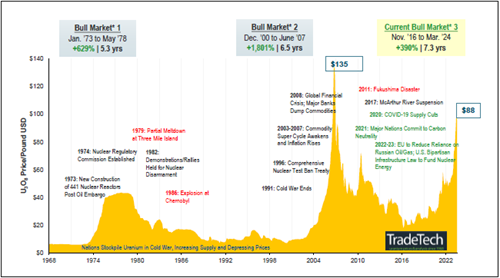

With global uranium mine production well short of the world’s uranium reactor requirements, the supply deficit building over the next decade, and near-term supply inhibited by long lead times and capital intensity, we believe that restarts and new mines in development are critical. The uranium price target as an incentive level for further restarts and greenfield development is a moving target, and we believe that we will likely need higher uranium prices to incentivize enough production to meet forecasted deficits. Over the long term, increased demand in the face of an uncertain uranium supply may continue supporting a sustained bull market (Figure 4).

Figure 4. Uranium Bull Market Continues (1968-2024)

Click here to enlarge this chart.

Note: A “bull market” refers to a condition of financial markets when prices are generally rising. A “bear market” refers to a condition of financial markets when prices are generally falling.

Source: TradeTech Data as of 03/31/2024. TradeTech is the leading independent provider of information on uranium prices and the nuclear fuel market. The uranium prices in this chart dating back to 1968 are sourced exclusively from TradeTech; visit https://www.uranium.info/.

Footnotes

| 1 | The U3O8 uranium spot price is measured by a proprietary composite of U3O8 spot prices from UxC, S&P Platts and Numerco. |

| 2 | The North Shore Global Uranium Mining Index (URNMX) was created by North Shore Indices, Inc. (the “Index Provider”). The Index Provider developed the methodology for determining the securities to be included in the Index and is responsible for the ongoing maintenance of the Index. The Index is calculated by Indxx, LLC, which is not affiliated with the North Shore Global Uranium Miners Fund (“Existing Fund”), ALPS Advisors, Inc. (the “Sub-Adviser”) or Sprott Asset Management LP (the “Adviser”). |

| 3 | The Nasdaq Sprott Junior Uranium Miners™ Index (NSURNJ™) was co-developed by Nasdaq® (the “Index Provider”) and Sprott Asset Management LP (the “Adviser”). The Index Provider and Adviser co-developed the methodology for determining the securities to be included in the Index and the Index Provider is responsible for the ongoing maintenance of the Index. |

| 4 | The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index that tracks prices of futures contracts on physical commodities, and is designed to minimize concentration in any one commodity or sector. It currently has 23 commodity futures in six sectors. |

| 5 | The S&P 500 or Standard & Poor's 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. |

| 6 | Source: World Nuclear Association. WNA Nuclear Fuel Report 2023.. |

| 7 | Source: Kazatomprom Investor Handout FY2023. |

| 8 | Source: Ur-Energy Announces Decision to Build Out Shirley Basin Mine. |

| 9 | Source: Ur-Energy Announces Decision to Build Out Shirley Basin Mine. |

| 10 | Source: enCore Energy Announces First Shipment and Delivery of Uranium; Continues to Address Critical Shortage of Domestic Uranium Supply to Fuel Nuclear Energy. |

| 11 | Source: Global Atomic Updates its Dasa Project Feasibility Study and Announces Off-Take Agreement. |

| 12 | Source: Washington Post, Niger junta announces end to military relationship with United States. |

| 13 | Source: Reuters, Last French troops leave Niger as military cooperation officially ends. |

| 14 | Source: Powermag.com, Palisades Nuclear Plant on Path to Recommissioning by 2025. |

| 15 | Source: France’s Orano studying plan to build U.S. uranium enrichment plant . |

| 16 | Source: Reuters, Nuclear fuel supple shift must cut reliance on Russia, says U.S. energy official. |

| 17 | Source: Bloomberg, Russia Uranium Supplier Warns US Clients to Brace for Export Ban. |

Important Disclosure

Past performance is no guarantee of future results. You cannot invest directly in an index. Investments, commentary and statements are that of the author and may not be reflective of investments and commentary in other strategies managed by Sprott Asset Management USA, Inc., Sprott Asset Management LP, Sprott Inc., or any other Sprott entity or affiliate. Opinions expressed in this commentary are those of the author and may vary widely from opinions of other Sprott affiliated Portfolio Managers or investment professionals.

This content may not be reproduced in any form, or referred to in any other publication, without acknowledgment that it was produced by Sprott Asset Management LP and a reference to sprott.com. The opinions, estimates and projections (“information”) contained within this content are solely those of Sprott Asset Management LP (“SAM LP”) and are subject to change without notice. SAM LP makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, SAM LP assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. SAM LP is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Sprott Asset Management LP. These views are not to be considered as investment advice nor should they be considered a recommendation to buy or sell. SAM LP and/or its affiliates may collectively beneficially own/control 1% or more of any class of the equity securities of the issuers mentioned in this report. SAM LP and/or its affiliates may hold a short position in any class of the equity securities of the issuers mentioned in this report. During the preceding 12 months, SAM LP and/or its affiliates may have received remuneration other than normal course investment advisory or trade execution services from the issuers mentioned in this report.

The information contained herein does not constitute an offer or solicitation to anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized or to any person to whom it is unlawful to make such an offer or solicitation. Prospective investors who are not residents of Canada or the United States should contact their financial advisor to determine whether securities of the Funds may be lawfully sold in their jurisdiction.

The information provided is general in nature and is provided with the understanding that it may not be relied upon as, or considered to be, the rendering of tax, legal, accounting or professional advice. Readers should consult with their own accountants and/or lawyers for advice on their specific circumstances before taking any action.

© 2024 Sprott Inc. All rights reserved.