The Sprott Physical Uranium Trust ("SPUT", TSX: U.U ($US); U.UN ($CA)) was launched just over a year ago, in July 2021. While we were optimistic about the prospects for uranium, we could not foresee the tectonic shifts in the uranium sector that followed the launch and SPUT's significant impact.

Looking back to SPUT's inception, uranium was emerging from a nine-year bear market (2011 to 2020). The spot uranium market was illiquid, inactive and opaque. Price discovery was a challenge and there was little investor interest in the sector despite an ongoing structural supply deficit that needed to be addressed to "keep the lights on". The spot market was characterized by a big supply surplus created by carry traders,1 while persistently low uranium prices created little incentive for utilities to accelerate fuel purchases under long-term contracts. In these market conditions, uranium enrichers were able to underfeed their operations, which added approximately 20 million pounds of annual uranium secondary supply to fill the gap in primary uranium production. For a sector as important as nuclear energy, this was the equivalent of operating on borrowed time. Moreover, many global governments were ignoring the benefits of nuclear power and sticking to plans to decommission existing nuclear reactors, which would have negatively impacted long-term demand.

SPUT has Helped Modernize the Physical Uranium Market

When Sprott acquired the Uranium Participation Corporation in July 2021 and reorganized it into the Sprott Physical Uranium Trust, this new investment vehicle acted as a catalyst for a market that was at a tipping point and needed a shot in the arm to move forward. SPUT helped to modernize the physical uranium market by providing enhanced transparency and disclosure. Sprott has focused on clear and consistent communication and committed significant resources to educate investors on the case for investing in physical uranium and the benefits of nuclear energy. Side note: Sprott's corporate head office is in Toronto, Ontario, Canada; Ontario is often cited as a leader in nuclear energy, generating approximately 58% of its electricity from this low carbon and reliable form of energy.2

The Sprott Physical Uranium Trust is the largest and only publicly-listed physical uranium fund currently in the marketplace.3

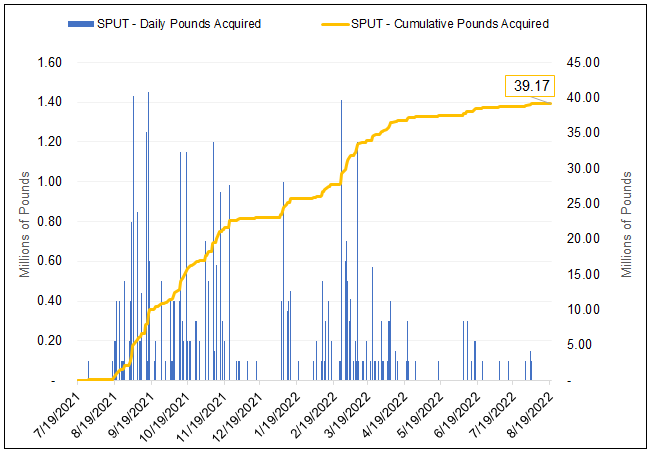

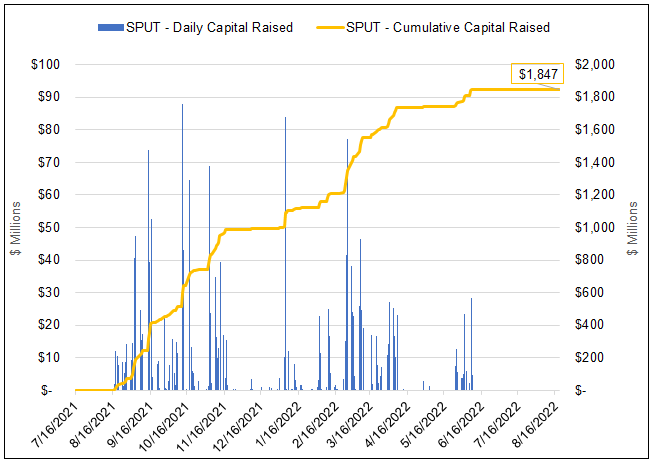

We believe that SPUT provides investors with an accessible investment that allows them to express their interest in physical uranium. SPUT has improved liquidity and price discovery in the uranium market and has attracted approximately US$1.85 billion in new capital since launch (Figure 1b). We have deployed these assets to acquire 39 million pounds of physical uranium in the spot market, as shown in Figure 1a. SPUT's 12-month growth represents more than 250 uranium purchases from 28 different counterparties. As of this writing (8/24/2022), SPUT held a total of ~57 million pounds of U3O8 and was valued at US$2.77 billion.

Sprott Physical Uranium Trust's Growth Since July 2021 Launch

Figure 1a. Uranium Pounds Purchased by SPUT

Figure 1b. $ Capital Raised by SPUT

Source: Sprott Asset Management LP. Data as of 8/19/2022.

The Changing Dynamics of the Uranium Market

Engineering a more accessible investment vehicle like the Sprott Physical Uranium Trust helped to ignite investor interest in physical uranium, but the key catalysts were market driven. Over the past year, sentiment towards nuclear energy has undergone a sea-change, driven by several factors.

The First Shift in Energy Policy: Transition

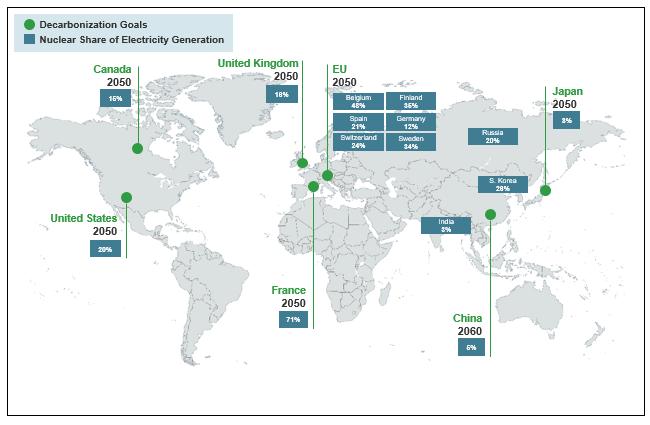

Global governments have set ambitious climate goals (Figure 2a) and it has become increasingly clear that these energy transition targets cannot be met without a reliable, low or zero-carbon-based energy source. For all the benefits of renewable energy sources like wind and solar, they face one major drawback – intermittency. Wind does not continuously blow, nor does the sun always shine, which means that a consistent energy source is required to support renewables.

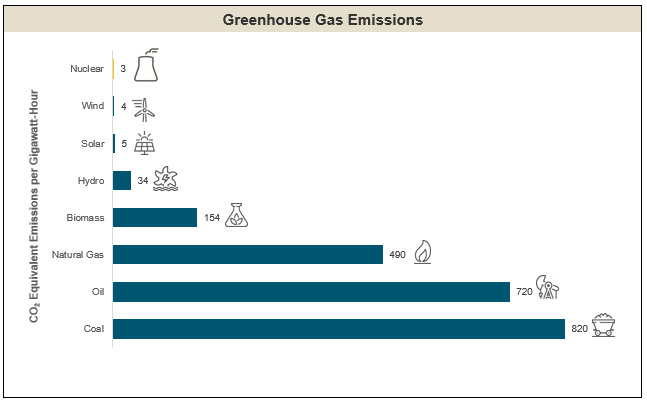

Nuclear power has the potential to fill this need, given that it has the highest capacity factor versus both traditional and alternative energy sources. In addition to providing a highly reliable source of electricity, nuclear power is one of the cleanest energy sources based on CO2 emissions (Figure 2b) and one of the safest energy sources available.4

Figure 2a. Global Decarbonization Goals Align with Nuclear Growth

Source: Carbon Neutrality by 2050: The World's Most Urgent Mission. Technical assessment of nuclear energy with respect to the 'do no significant harm' criteria of Regulation (EU) 2020/852 ('Taxonomy Regulation'). World Nuclear as of 12/31/2020.

Figure 2b. Nuclear Power is a Clean Energy Source

Nuclear energy produces the least CO2 equivalent emissions versus other energy forms, helping solidify its place in global decarbonization goals.

Source: Ourworldindata.org; measured in emissions of CO2-equivalent per gigawatt-hour of electricity over the lifecycle of the power plant. Data as of 12/31/2020. Also: https://www.world-nuclear.org/information-library/energy-and-the-environment/carbon-dioxide-emissions-from-electricity.aspx

The changing view of nuclear power became evident in 2021 at the United Nations Climate Change Conference (COP26, held in Glasgow from October 31 to November 13, 2021), where participating countries signed the Glasgow Climate Pact. This pact "calls on Parties to accelerate the development, deployment and dissemination of technologies, and the adoption of policies, to transition towards low-emission energy systems, including by rapidly scaling up the deployment of clean power generation." This major development was followed by the U.S. rejoining the Paris Climate Accord in January 2022 and the Biden administration announcing financial support for nuclear energy producers and utilities.

While nuclear had a negative halo in the years following Japan's Fukushima incident, mainstream media outlets have increasingly advocated that nuclear should play a larger role in electricity production. This message has received growing levels of support globally from individuals, businesses and policymakers. Nuclear's announced inclusion in the European Union's (EU) sustainable finance taxonomy in 2022 has signaled that European governments (except for some long-term holdouts) have finally accepted that nuclear power must be a key component of future energy policies.

Figure 3a. Nuclear Energy Sentiment is Improving Worldwide

Dates of Publication: POWER, 7/5/2022; Financial Times, 10/15/2021; CNBC, 8/19/2022; Forbes, 8/22/2022; Fortune, 11/15/2021; Bloomberg, 6/16/2022; The Wall Street Journal, 8/16/2022.

Figure 3b.

Positive Shifts in Favor of Nuclear Power are Accelerating |

|

The Second Shift in Energy Policy: Security

The start of 2022 brought optimism that we were in the late stages of the COVID-19 pandemic and that life would return to normal after two extremely stressful years. This optimism was short-lived when Russia invaded Ukraine on February 24, 2022. Instead of moving forward, we seemed to be moving back to an era we all wished would not return. The events unfolding in Ukraine for those directly impacted are tragic. The economic consequences of the conflict have touched most of us. Energy and commodity markets are global and their delicate balance has been disrupted.

Facing a shortage of natural gas, many countries, including those with historically "green" governments, have been forced to increase their reliance on coal for energy generation, which has negatively impacted climate goals and reinforced the need for more resilient energy policies. Countries like Germany are a case study for dysfunctional energy policies that have left them wondering whether they will have enough natural gas to heat their homes this winter. Relying on Russia for natural gas and oil and intermittent renewables for power generation has proven to be a losing strategy. In our view, the planned closing of the last of Germany's nuclear plants in 2021 and 2022 seems misguided. The Russia-Ukraine war and long-term energy policy failures have placed Europe in such dire straits that energy rationing seems inevitable. The economic and social impacts of these energy shortages are likely to be profound and far-reaching.

Once again, geopolitics have affected energy security and highlighted the importance of energy sovereignty and security. Unfortunately, politicians often need negative events to galvanize public support and move forward with difficult policy shifts.

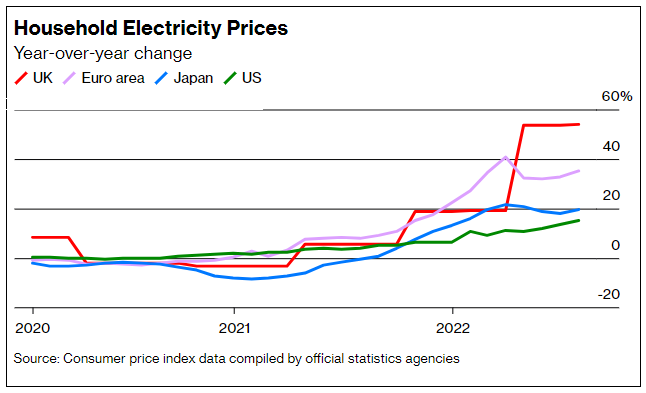

Figure 4. Worldwide Soaring Energy Prices (2020-2022)

Source: Bloomberg, 8/23/2022: A ‘Tsunami of Shutoffs': 20 Million US Homes Are Behind on Energy Bills.

Is Past Prologue?

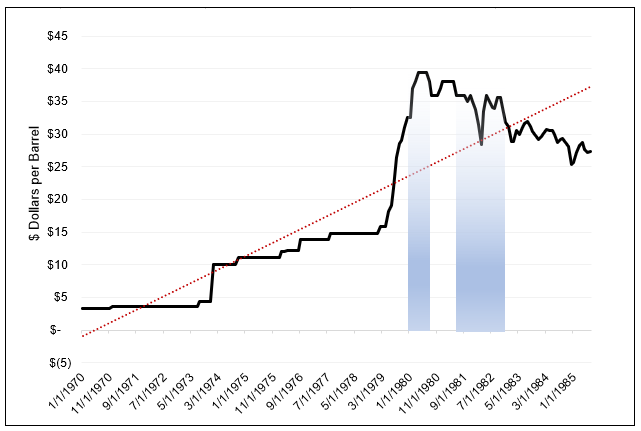

The energy crisis in 1973, spurred by OPEC (Organization of the Petroleum Exporting Countries), resulted in a major energy policy pivot in the West. The crisis galvanized political support for nuclear energy and prompted the buildout of many new nuclear power plants (NPPs). These plants continue to operate today and provide reliable and carbon-free electricity. We believe that the current global energy crisis is likely to help extend the lives of many of these nuclear power plants, which may contribute to increased demand for physical uranium.

Figure 5. Crude Oil Prices (1970 to 1985)

Shaded blue areas represent recessions.

Source: Federal Reserve Bank of St. Louis.

Globalization: The Hidden Risks of the Lower-Cost Option

The world has gone through a great period of globalization over the past 30 years, creating tremendous economic efficiencies and wealth for select countries, businesses and individuals. Certain industries and businesses were outsourced to lower-cost jurisdictions. A sizeable portion of the nuclear fuel supply chain was outsourced as the uranium bear market increased the attractiveness of lower-cost jurisdictions. Upstream, uranium mining in many countries contracted and even disappeared in the U.S., despite the U.S. having the world's largest fleet of nuclear reactors. Downstream, the situation worsened as Western utilities became increasingly dependent on low-cost Russian conversion and enrichment services.

Only as Strong as the Weakest Link? Reliance on Russia

Russia — accused of war crimes, violating basic human rights and weaponizing energy commodities — is now seen as the weakest link in the global nuclear supply chain, and the West is now paying the price. While Russia is not a significant producer of uranium, it accounts for a meaningful portion of global capacity for uranium conversion and enrichment services. Western utilities are facing a conundrum: How to shift away from Russian conversion and enrichment services when alternatives are not readily available?

The lack of available capacity was a direct result of the protracted uranium bear market that drove prices to uneconomical levels and forced several key operations, such as ConverDyn's Illinois facility to go offline in 2017. Despite the recent increase in prices across the nuclear fuel supply chain, Western conversion and enrichment facilities have indicated they will not ramp up capacity until an appropriate and durable incentive price is reached and, more importantly, not until appropriately priced long-term contracts are in place with major utilities.

The U.S. government has belatedly begun efforts to wean the U.S. off its reliance on Russia for nuclear fuel services and enrichment capacity. Two draft bills are currently working their way through Congress and the Biden administration has requested $4.3 billion in funds to support domestic uranium mining and nuclear fuel chain services. However, these measures are clouded by uncertainties. Will Russia act first and impose countermeasures against the West? Will the price of uranium increase to an incentive level and prompt the reopening of North American uranium mines? The U.S. Inflation Reduction Act of 2022 includes various incentives for the clean energy sector, including tax incentives for operating nuclear power plants, advanced reactors, clean energy manufacturing and funding for high-assay low-enriched uranium (HALEU). Some pundits have estimated the value of the nuclear sector at $30 billion. Source: Canaccord, Analyst Katie LaChapelle, August 8, 2022.

Figure 6. More Countries are Embracing Nuclear Energy

| Expanding Nuclear Energy | Shifting Back to Nuclear Energy | Exploring Nuclear Energy for First Time |

|

|

|

Source: UxC Nuclear Power Developments Review as of 6/24/2022.

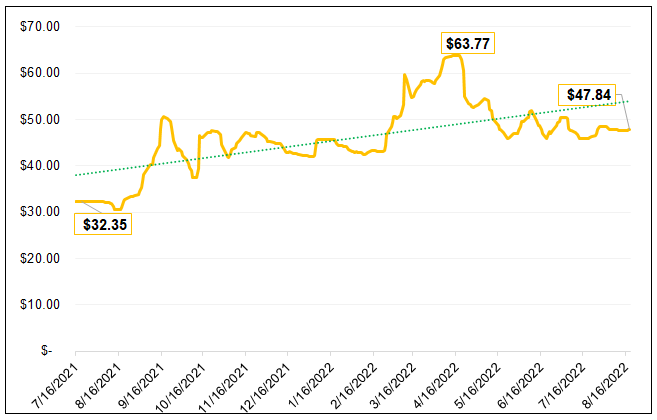

Final Thoughts: The Uranium Bull Market Remains Intact

Over the past year, the Sprott Physical Uranium Trust's investors have often asked whether we have reached a true inflection price for uranium or if its recent rise is just another false start. While we cannot predict the future, we believe the sector is finally emerging from its multi-year bear market (Figure 7). We continue to believe that nuclear is going to play a larger role in the global energy transition and that over time this will lead to a trend of potentially higher uranium prices. Despite the recent macro headwinds impacting most asset classes, we believe the uranium bull market remains intact.

Figure 7. The Uranium Spot Price since Sprott Physical Uranium Trust Launch

Source: The uranium spot price is measured by a proprietary composite of U3O8 spot prices from UxC, S&P Platts and Numerco. Data as of 8/19/2022.

The Sprott Physical Uranium Trust has transformed the uranium market by creating what we believe is a preferred vehicle for investors to obtain exposure to physical uranium. The influx of capital and the effect on the market have removed the spot supply overhang and provided a supportive environment for uranium mining companies to make more confident long-term production decisions. Uranium mining companies are critical partners to the utilities and the nuclear energy ecosystem. Both sides need a healthy industry to ensure a secure long-term fuel supply. We have been encouraged by the growing signs that the sector is returning to stronger, more certain times. A new long-term supply contracting cycle is underway, as highlighted by Cameco's 75 million pounds of uranium contracted from the beginning of 2021 to the present.

The planned restarts of several idle mines operated by Cameco, Paladin Energy and Boss Energy are the first steps to bringing the uranium market back to equilibrium. Investor capital has finally returned to the sector after a multi-year drought. For example, we are seeing the development of tier-one uranium deposits from companies such as NexGen Energy, including its highly anticipated greenfield Rook I project in the southwest Athabasca Basin, Saskatchewan. Uranium exploration companies are active again, searching for future deposits that will replace existing mines.

The global push for decarbonization and electrification has been in the making for some time, but it is only starting to take off. Targets are becoming policies, and policies are becoming law. In our view, the future for uranium and nuclear energy has never been brighter. In a year that has seen more positive changes to the uranium and nuclear industry than in the previous decade, the entrance of the Sprott Physical Uranium Trust is regarded as one of the more significant events over the last 12 months.

| 1 | Carry trades are considered an off-balance sheet financing agreement between a trader and a utility, in which the utility commits to buy material at a predetermined price on a future date. In an oversupplied market, where there is excess spot material, it is often cheaper to buy material today and carry it than to pay producers to mine it in the future. |

| 2 | The World Nuclear Association. Data as of 2021. |

| 3 | Based on Morningstar’s universe of listed commodity funds as of 6/30/2022. |

| 4 | Based on comparative death rates reported by Markandya & Wilkinson (2007) in The Lancet, and Sovacool et al. (2016) in Journal of Cleaner Production. |

Important Disclosure

* Sprott Physical Uranium Trust is the world's largest physical uranium fund based on Morningstar’s universe of listed commodity funds. Data as of 6/30/2026.

Sprott Physical Uranium Trust (the “Trust”) is a closed-end fund established under the laws of the Province of Ontario in Canada. The Trust is generally exposed to the multiple risks that have been identified and described in the prospectus. Please refer to the prospectus for a description of these risks. Relative to other sectors, precious metals and natural resources investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage, and liquidity should also be considered.

All data is in U.S. dollars unless otherwise noted.

Past performance is not an indication of future results. The information provided is general in nature and is provided with the understanding that it may not be relied upon as, nor considered to be tax, legal, accounting or professional advice. Readers should consult with their own accountants and/or lawyers for advice on their specific circumstances before taking any action. Sprott Asset Management LP is the investment manager to the Trust. Important information about the Trust, including the investment objectives and strategies, applicable management fees and expenses, is contained in the prospectus. Please read the prospectus carefully before investing.The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or operational charges or income taxes payable by any unitholder that would have reduced returns. You will usually pay brokerage fees to your dealer if you purchase or sell units of the Trust on the Toronto Stock Exchange (“TSX”). If the units are purchased or sold on the TSX, investors may pay more than the current net asset value when buying units of the Trust and may receive less than the current net asset value when selling them. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated. The information contained herein does not constitute an offer or solicitation to anyone in the United States or in any other jurisdiction in which such an offer or solicitation is not authorized.