Video Transcript

Rare Earths: Indispensable to the Modern World

Rare earth elements are increasingly making headlines, not only in financial media but also in the mainstream press, and for good reason. These 17 chemically similar metallic elements have remarkable magnetic, luminescent and electrochemical properties, and are superb catalysts in a variety of chemical processes, making them indispensable to our modern world.

Rare earths aren’t exactly rare. In fact, they occur in the earth’s crust in greater abundance than many common minerals, but they are rarely found in the same location and exceedingly difficult to economically mine and process, making finished rare earth materials tough to come by.

And this is a problem, because they are vital to the manufacturing of thousands of products across the defense, technology and energy sectors, including electronics, AI data centers, and more. Further compounding the challenge of extracting and refining rare earths is the fact that China controls most of the world’s supply chain, with a stranglehold on most of both mining and processing.

In a time when the geopolitical landscape is rapidly shifting beneath our feet and the world is bifurcating into a multipolar reality, one country having this level of unprecedented, standalone access to such an important commodity is why rare earths have become a hot topic in recent times.

However, where there is uncertainty, there can also be opportunity. That’s why the U.S. and other governments outside China are bringing much-needed domestic supplies online, in an effort to swing the pendulum of access to rare earths closer to the West and to a growing global demand that shows no signs of slowing.

What are Rare Earth Elements?

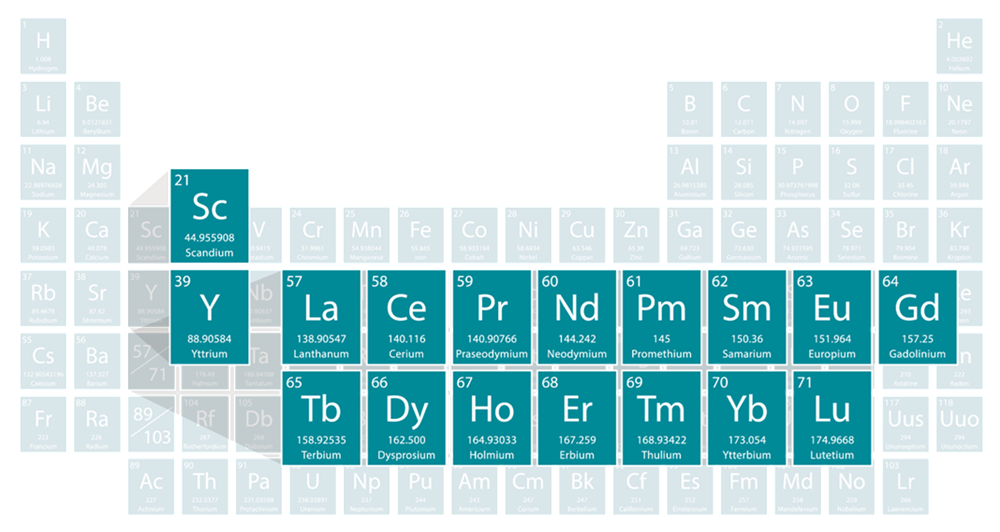

Of the 17 elements that make up the rare earth family, 15 are called “lanthanides”, starting on the periodic table with lanthanum and ending with lutetium. Unlike most other elements, where outer electrons often change dramatically and create big differences in properties, lanthanides share strikingly similar chemical behaviors, and this is one of the main reasons they’re so difficult and expensive to mine and process, as separating elements with such similar characteristics is an incredibly delicate task.

The other two elements are scandium and yttrium, very similar to the 15 lanthanides, but with certain properties, including a lack of f-electrons, which cause them to fall into a subcategory of their own.

Rare earths are also categorized as light or heavy, according to their atomic mass. We won’t dive too deep into the science behind this, but suffice to say that light rare earths are more common and less in demand, while their heavy rare earth counterparts are scarcer and highly sought after for advanced, high-performance technology.

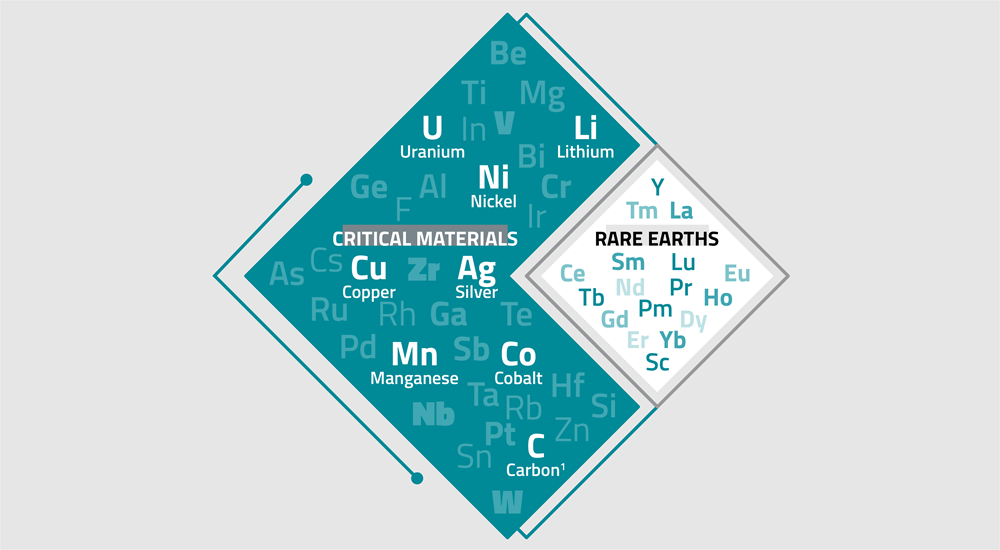

One important thing to note: while some people use the terms rare earths and critical minerals interchangeably, the term “critical minerals” refers to a broader range of natural resources deemed essential for economic stability and national security, with rare earths making up a subset of critical minerals, alongside uranium, silver, copper and many other elements.

In industrial applications, the largest and fastest-growing segment is permanent magnets, which account for over 80% of global demand by value. Rare earths such as neodymium, praseodymium, dysprosium, terbium, and samarium are used to create amazingly powerful, lightweight, and compact magnets that retain their magnetic strength even at unusually high temperatures.

Rare earths also function as catalysts. Cerium and lanthanum are central to petroleum refining and automotive emission control via catalytic converters, rubber and polymer production, environmental and industrial waste treatment, energy and fuel cell applications, and many other applications.

Rare earth elements are also used to illuminate display screens on a variety of digital devices, to create steel and aluminum, in battery technology, military defense technology (which we’ll home in on a little later) and in medical devices and healthcare. The list goes on.

As the AI arms race accelerates and data center buildouts advance rapidly, rare earths are also playing a vital role in shaping the artificial intelligence landscape.

Figure 1. REEs are a Subset of Critical Materials

* Note: Graphite—reflected in Sprott’s list of critical materials focus—is an allotrope of Carbon.

Source: Sprott Asset Management.

Rare Earths and the AI Revolution

The race to be the leader in artificial intelligence is fully underway, and tech industry giants, alongside government leaders and major financial backers, are advancing rapidly in a high-stakes game where the winner could reshape cybersecurity, economic growth, and military technology forever.

The main competitors are the United States and China, but countries around the globe have thrown their hats into the ring to avoid being left behind as AI tech continues to evolve at a breakneck pace.

Rare earth elements are absolutely essential to the AI revolution, for a variety of reasons. Neodymium-iron-boron permanent magnets, often alloyed with dysprosium and terbium for heat resistance and praseodymium for added strength, are an essential component of the massive hard disk drives needed for AI’s insatiable data storage requirements.

Cooling systems, often accounting for up to 50% of a data center’s electricity requirements, need to be ultra-efficient to counteract the enormous heat generated by AI servers, and powerful permanent magnets made with rare earths are needed in fans, cooling pumps, and actuators.

Rare earths are also indispensable for semiconductor manufacturing, with cerium oxide needed to polish silicon wafers to atomic-level flatness before etching nanoscale circuits in GPUs and AI accelerators. Yttrium is used to modify the electrical and magnetic properties of semiconductor compounds, enabling better power efficiency and improved transistor control in high-performance AI processors.

Terbium and praseodymium are vital for amplifiers, optical isolators, and components in high-speed fiber-optic networking. Rare earth magnets once again come into play to support motors in robotic server-maintenance systems, uninterruptible power supplies, and backup generators, and some AI systems also make use of rare earths in power-supply components or thermal interfaces for stable operation under heavy AI energy loads.

Going back to our earlier point about China’s dominance of rare earth supply chains, the United States Geological Survey estimates that approximately 80% of rare earths for magnets, storage, and related components used for AI in the United States are reliant on imports, with the vast majority coming from China, a statistic that should concern policy makers and political leaders, and a driving force behind the search for non-Chinese production and processing.

Of course, the key input for AI data centers is energy, and rare earth elements play a role in that department as well.

Rare earths are used in permanent magnets embedded in the rotors of permanent-magnet synchronous generators, which are used in most modern wind turbines. These magnets enable higher efficiency, lower weight, and fewer moving parts than traditional geared systems or electromagnetic generators.

In addition, light rare earths such as lanthanum and cerium are used in traditional hydrocarbon-based energy generation, as petroleum-refining catalysts and for fluid catalytic cracking, operations that improve the crude oil-to-fuels process for powering coal- and gas-fired electricity plants.

Rare earths such as gadolinium are used in the nuclear energy sector. This rare earth element is often mixed into uranium oxide pellets to suppress initial excess reactivity in fuel assemblies, allowing longer fuel cycles and higher burnup while preventing power spikes.

Dysprosium and europium are used in control rods for day-to-day power regulation or emergency shutdown. Samarium is also used in control rods, along with burnable absorbers, and various rare earths are employed to improve fuel performance and corrosion resistance, neutron radiation shielding, and more.

As artificial intelligence and its incredible power requirements drive rare earth demand, the defense sector is another area where they are needed more than ever, as defense spending and militarization ramp up in an increasingly divided geopolitical landscape.

Rare Earths on the Frontlines of Next Gen Warfare

Did you know that NATO identifies Rare Earth Elements as part of its 12 defense-critical raw materials, with the majority of them being classified as high risk in regard to securing supply? There’s a good reason for this: many rare earths are absolutely essential for military tech, and as global conflict continues to escalate, unfettered access to a reliable source of materials is non-negotiable. In addition, the nature of warfare is changing, leaning less on boots-on-the-ground battles and more on drone and missile-based operations, meaning secure access to rare earths is mission-critical.

Military drones require efficient, compact, lightweight electric motors, sensors, and actuators, which are achievable only with high-performance permanent magnets made with rare-earth materials. These magnets, primarily neodymium-iron-boron but sometimes the tougher samarium-cobalt, are the gold standard for producing drones that can operate under the brutal conditions of modern warfare, including extreme vibrations, temperature swings from minus 55 degrees Celsius all the way up past 125, and to altitudes pushing 50,000 feet.

Rare earths are also required for missile guidance and control systems, as they enable pinpoint precision and enhanced maneuverability through the same cutting-edge permanent magnet technology used in drones. These magnets power actuators and motors that control the missile’s fins and flight surfaces, delivering exceptional torque and power density while resisting extreme heat, vibrations, and G-forces during launch and flight. Without these magnets powered by rare earths, “smart” guidance in the missiles would fail, eliminating the ability to make rapid course corrections en route to their targets.

Neodymium and yttrium are employed in rangefinders, target designators, and illuminators on tanks, aircraft, and portable infantry systems, allowing for effective targeting at ranges in the tens of miles, and yttrium-based materials are also used to tune radar and sonar frequencies for increased resolution and threat detection.

There are other especially important military applications for rare earths, including in night vision goggles, communications technology, satellites and space systems, mine detection, and more. Suffice to say, rare earths form the backbone of modern military tech, and that’s not about to change anytime in the foreseeable future.

Underlining this burgeoning demand is the increase in national defense budgets all over the world. In fact, the International Institute for Strategic Studies has concluded that global defense spending hit record levels in 2025, reaching approximately $2.63 trillion, up 2.5% in real terms from 2024, part of a multi-year trend driven by rising global conflicts and geopolitical uncertainty that is expected to continue.

Over 100 countries have increased their military spending in recent years, and the majority of those are European states and NATO member nations, precisely the kinds of countries that are looking for rare earth supplies from outside of China. All 32 NATO-member nations met their 2% of GDP military spending guidelines for the first time in 2025, and the organization has set a goal of 5% of GDP for military spending by 2035, a figure that could dramatically increase demand for rare earth elements in the years ahead.

With the massive importance of breaking away from China’s dominance of rare earths production and processing looming large, that begs the questions: how did China get so much control over the industry to begin with, and just how big a risk does this present to non-allied nations?

China’s Dominance of Rare Earth Supply Chains

China has many advantages in the natural resource sector that are undeniable: a low cost of labor, a state-controlled economy that allows for less red tape and faster permitting times, and a long-term strategy enabled by a lack of public elections, which allows political leaders to advance agendas without having to cater to any particular voter base. As part of this long-term strategy, China has made tremendous strides in forming global partnerships in the resource sector and nowhere are all these factors more evident than in the rare earth elements business.

Many don’t realize the United States used to be the dominant player in the rare earths industry, from around 1960 until the early 1990s, but could not compete with China in the face of increased environmental scrutiny at home, and the undeniable advantages just discussed. In 1992, then-leader of China, Deng Xiaoping, declared, "…the Middle East has oil, China has rare earths."

China now accounts for approximately 70% of rare earth mining and a staggering 90% of refining. This presents some serious risks for countries that are on the opposite end of rare earth trade negotiations with the Chinese Communist Party (CCP).

When rare earths are needed for so many modern military tech applications and you rely on China for those rare earths, that reliance is a weapon that can be wielded to devastating effect by choking supply lines and restricting access. This is a tactic China has already used on several occasions, including their recent export controls on seven medium and heavy rare earths, including their compounds, metals, alloys, and downstream products such as permanent magnets, instituted by the Ministry of Commerce in April 2025. This requires state approval for exports, a process that is often time-consuming, opaque and often results in pricing so high that rare earth exports from China—to be used in U.S. military tech—are effectively banned.

China further escalated in October 2025 by extending controls across the entire rare earth supply chain and adding other critical minerals. Following a Trump-Xi meeting in November 2025, many of these expanded measures were suspended for one year, though this is a temporary pause. The prior export controls remain fully in effect, and the military end-user ban was never lifted.

These kinds of policies can have a major impact on price levels as well, as evidenced by the export controls placed on rare earths by China in 2010, where they cut off shipments to Japan, resulting in an astounding 26-fold price spike in several rare earth elements between January 2009 and August 2011.

As geopolitical tensions rise around the globe, the chance of China further tightening export restrictions on rare earths is a reality all political leaders and policy makers are acutely aware of, but the question remains: what steps can be taken to reduce and even remove dependence on China when it comes to rare earth supply chains?

Policy Catalysts for Non-Chinese Rare Earths Supply

The positive side of Chinese export controls being implemented on rare earths is the awareness it has spread to governments, militaries, and companies that rely on rare earths, and this has resulted in several policy initiatives to encourage non-Chinese production and processing.

Rare earths are now a key component of critical minerals lists released by governments around the world and are often cited as a high priority in terms of national security. Now it’s one thing to categorize rare earths as important, but what concrete steps are being taken to establish new sources of rare earth supplies?

The United States and Australia have signed a framework as of October 2025, which includes rare earth mining, separation, and processing, in a bid to secure diversified supply chains for both nations. This includes a minimum one billion dollar commitment within the first six months, the acceleration, streamlining, and deregulation of permitting to cut red tape and get the minerals out of the ground, price mechanisms such as floor pricing, and to top it off, the U.S. Export-Import Bank has issued four letters of interest for the framework, which could lead to around 800 million dollars of investment into Australian rare earth projects.

Japan and the U.S. have also signed on to a bilateral partnership designed to strengthen supply chains of critical minerals and reduce dependency on foreign nations such as China for rare earths and includes joint investments, coordinated policy, and technology-sharing to meet this goal.

In addition, the U.S. launched Project Vault in February of 2026, one of the most ambitious critical minerals stockpiling initiatives for the country to date, earmarking 12 billion dollars through a public-private partnership to create a strategic reserve of critical minerals, including rare earths.

On the European side, the EU has established the Critical Raw Materials Act, as of 2024, along with the more recent RESourceEU Action Plan in 2026, both created to diversify critical materials, including rare earths, away from China and towards domestic and allied sources. These initiatives look to accomplish several objectives, including 10% of the bloc’s annual strategic raw materials consumption to be from EU sources, 40% from domestic processing, and 25% from recycling by 2030, along with mobilizing approximately 3 billion euros over a 12-month period to fast track 25 to 30 strategic projects in the region, and a stockpiling pilot program led by France, Germany, and Italy to establish strategic reserves of critical minerals for EU member states.

The U.S. Department of Defense has locked in above-market floor pricing for the procurement of rare earth materials from American producer MP Materials, along with Japan Australia Rare Earths, a Japanese government organization, locking in a separate floor pricing contract at above-rate levels with Australian rare earth producer Lynas.

These price floors can play a key role in reducing volatility and improving planning certainty, a game changer in the highly volatile market of commodities extraction, which may facilitate greater profitability and investment for scaling up future capacity.

The Sprott Rare Earths Ex-China ETF

Given everything we’ve outlined so far, the potential opportunity in the rapidly developing rare earth supply chain outside of China could be a game changer for the natural resource investment landscape.

Sprott Rare Earths Ex-China ETF (Nasdaq: REXC) offers investors targeted exposure to rare earth companies outside of China, positioned to benefit from rising demand and investment in global supply chain realignment. REXC is the only1 ETF providing focused, pure-pure play2 exposure to rare earth companies.

About Jesse Day

Jesse Day is a video producer and writer with a focus on commodities and natural resources. Jesse’s vision for Commodity Culture is to provide education to anyone interested in exploring the delicate balance of commodities and the vital role they play in our economy and our lives. Jesse studied film at Capilano University and currently works as Communications Coordinator at Kin Communications Investor Relations in Vancouver. Jesse has also had a fairly long career in broadcasting in Asia, having hosted a variety of travel programs in China and South Korea.

Find out more about Sprott Rare Earths Ex-China ETF.

Footnotes

| 1 | Based on Morningstar's universe of Natural Resources Sector Equity ETFs as of 4/14/2026. |

| 2 | The term “pure play” relates directly to the exposure that the Fund has to the total universe of investable, publicly listed securities in the investment strategy. |

Jesse Day is not an employee or an affiliate of Sprott Asset Management LP. The opinions, estimates and projections ("information") contained within this content are solely those of the presenter and are subject to change without notice. Sprott Asset Management LP makes every effort to ensure that the information has been derived from sources believed to be reliable and accurate. However, Sprott Asset Management LP assumes no responsibility for any losses or damages, whether direct or indirect, which arise out of the use of this information. Sprott Asset Management LP is not under any obligation to update or keep current the information contained herein. The information should not be regarded by recipients as a substitute for the exercise of their own judgment. Please contact your own personal advisor on your particular circumstances. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds managed by Sprott Asset Management LP. These views are not to be considered as investment advice nor should they be considered a recommendation to buy or sell.

Important Disclosures & Definitions

An investor should consider the investment objectives, risks, charges, and expenses carefully before investing. To obtain a Sprott Rare Earths Ex-China ETF Statutory Prospectus, which contains this and other information, visit https://sprottetfs.com/rexc/prospectus, contact your financial professional or call 888.622.1813. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the funds, typically in blocks of 10,000 shares.

The Sprott Rare Earths Ex-China ETF and the Sprott Active Metals & Miners ETF are new and have limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott Rare Earths Ex-China ETF. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.