Sprott Focus Trust

Manager Commentary December 31, 2025

Whitney George

The following commentary covers the 12-month period from January 1 - December 31, 2025, and is an excerpt from the Sprott Focus Trust 2025 Annual Report.

January 28, 2026

Dear Fellow Shareholders,

2025 was a good year for Sprott Focus Trust (FUND). FUND’s Net Asset Value (NAV) appreciated 23.57% and FUND’s market price posted a total return of 27.55%. This compares very favorably to the 17.15% total return for the Russell 3000 Index. In addition, FUND paid distributions of $0.577 per share and repurchased 1,542,087 shares at an average price of $7.63 during 2025.

As we predicted a year ago, 2025 was a volatile year. The year began on an upswing, but then equity markets drew down aggressively on tariff news in the spring. As the U.S. government pushed off “Liberation Day” tariffs, stock markets rallied, closing out the year with solid gains. However, beneath the surface, an important news theme emerged which we have long been prepared for: “The Debasement Trade”. This is most clearly observed in the rising price of gold during 2025.

The Debasement Trade

Gold began the year at approximately $2,600 per ounce, then rose and settled around $3,300 from April to July. In late August, precious metals resumed their advance with urgency, driven by what is now widely called the “Debasement Trade”, reflecting the shift of capital out of fiat currencies (notably the U.S. dollar) and sovereign debt into scarce, “hard” assets, driven by fear that both massive government spending and debt monetization are devaluing money. While the U.S. administration’s attack on the Federal Reserve’s independence was a clear headline, a much broader global concern emerged. In early October, gold broke above its inflation-adjusted high of $3,900 on news of a new Japanese Prime Minister and the third French Prime Ministerial resignation in three months. As Paul Wong, Sprott Managing Partner and Market Strategist, noted, Japan is often viewed as a bellwether of structural macroeconomic trends for Western markets due to its loose monetary policy, high debt and aging demographics. There are also many financial market linkages, such as the yen carry trade, capital flows and asset allocation by massive Japanese pension funds and insurers.

Japan’s new Prime Minister Takaichi is considered an “Abenomics” disciple. The three pillars of former Prime Minister Abe’s economic plan were: 1) aggressive monetary policy (i.e., Zero Interest Rate Policy [ZIRP] and Negative Interest Rate Policy [NIRP]); 2) flexible fiscal policy (huge stimulus); and 3) structural reforms (deregulation). The main macro takeaway from Abenomics was that fixed-income yields were forced lower, the yen weakened and equity markets soared. In the case of France, the second-largest member of the European Monetary Union (but not a fiscal union), the country continues to be a source of stress episodes. Fearing global monetary and fiscal policies would drive ever-rising sovereign debt levels, investors sought safety in hard assets like precious metals.

Gold’s signal was confirmed by the price of many other commodities and hard assets in general in the fourth quarter of 2025. In our view, FUND is very well positioned for this rotation and is off to a very strong start in 2026, up 11.97% as of this writing.

Positioning and Portfolio Activity

From year-end 2024 to year-end 2025, FUND’s portfolio remained deliberately concentrated (32 equity holdings at both year-end dates), with roughly the same structure: 19 holdings accounted for at least 75% of invested assets as of 12/31/2025, versus 20 holdings as of 12/31/2024. This illustrates FUND’s discipline of focusing capital on the best ideas, even as the mix may evolve.

The most visible shift over the year was in cash deployment. Cash and cash equivalents declined from about 7.8% of net assets as of 12/31/2024 to about 4.9% as of 12/31/2025, moving from FUND’s largest line item in 2024 to one of several similarly sized top positions in 2025. This coincided with an increase in FUND’s net assets from roughly $251 million to $287 million, while the portfolio’s weighted average P/E fell from 13.7x to 12.5x, as we continue to focus on value.

Sector exposures also became more purposeful. Materials increased from about 38.4% to 40.6%, Energy from 13.8% to 15.1%, and Consumer Discretionary from 9.1% to 12.4%, while Real Estate fell meaningfully from 9.1% to 6.1%. Geographically, FUND’s portfolio became more globally balanced, with U.S. exposure falling from 68.7% to 60.5%.

At the individual position level, the 2025 top weights were tightly clustered (generally 4% to 5%), led by Nucor Corporation, ASA Gold and Precious Metals Limited, Steel Dynamics, Inc., Helmerich & Payne, Inc. and Major Drilling Group International Inc. FUND’s portfolio shifted from a 2024 profile where cash dominated and a handful of holdings sat just under 5%, to a 2025 profile where multiple cyclically geared businesses (steel, drilling services, energy) and precious metals sensitivity shared top billing. This helped align exposures with the year’s strongest performance drivers: Materials was the largest positive sector contributor in 2025, and several precious metals-linked holdings were among the top individual contributors.

Figure 1

Top 10 Positions as of 12/31/20251 (% of Net Assets)

| Nucor Corporation | 4.9 |

| ASA Gold and Precious Metals Limited | 4.9 |

| Steel Dynamics, Inc. | 4.8 |

| Helmerich & Payne, Inc. | 4.7 |

| Major Drilling Group International Inc. | 4.6 |

| Federated Hermes, Inc. | 4.4 |

| Reliance, Inc. | 4.3 |

| Exxon Mobil Corporation | 4.2 |

| Cal-Maine Foods, Inc. | 4.2 |

| The Buckle, Inc. | 4.1 |

| Top 10 Total | 45.1 |

Holdings may vary, and this list is not a recommendation to buy or sell any security.

Figure 2

Portfolio Sector Breakdown as of 12/31/20251 (% of Net Assets)

| Materials | 40.6 |

| Energy | 15.1 |

| Consumer Discretionary | 12.4 |

| Financial Services | 10.7 |

| Real Estate | 6.1 |

| Cash & Cash Equivalents | 4.8 |

| Consumer Staples | 4.2 |

| Industrials | 3.8 |

| Technology | 2.3 |

| Total | 100 |

1 Sector weightings are determined using the Bloomberg Industry Classification Standard (“BICS”).

Figure 3

Portfolio Diagnostics

| Fund Net Assets | $287.3 million |

| Number of Equity Holdings | 32 |

| 2025 Annual Turnover Rate | 17.41% |

| Net Asset Value | $9.61 |

| Market Price | $8.68 |

| Average Market Capitalization1 | $4.73 Billion |

| Weighted Average P/E Ratio2,3 | 12.54x |

| Weighted Average P/B Ratio2 | 1.84x |

| Weighted Average Yield | 2.94% |

| Weighted Average ROIC | 19.97% |

| Weighted Average Leverage Ratio | 1.81x |

| Holdings ≥75% of Total Investments | 19 |

| U.S. Investments (% of Net Assets) | 60.51% |

| Non-U.S. Investments (% of Net Assets) | 39.49% |

| 1 | Geometric Average. This weighted calculation uses each portfolio holding’s market cap in a way designed to not skew the effect of very large or small holdings; instead, it aims to better identify the portfolio’s center, which Sprott believes offers a more accurate measure of the average market cap than a simple mean or median |

| 2 | Harmonic Average. This weighted calculation evaluates a portfolio as if it were a single stock and measures it overall. It compares the total market value of the portfolio to the portfolio’s share in the earnings or book value, as the case may be, of its underlying stocks. |

| 3 | Fund’s P/E ratio calculation excludes companies with zero or negative earnings (18.62% of holdings as of 12/31/2025). |

Over the course of 2025, we kept FUND’s portfolio concentrated and focused, while making a few intentional changes at the edges where we saw better risk-adjusted opportunities. By year-end, we had initiated three new positions: SLB, Gentex Corporation and H&R Block, Inc. We added SLB to broaden and improve the quality of our energy services exposure, giving FUND a globally diversified way to participate in sustained upstream activity without relying solely on commodity price direction. We initiated a position in Gentex to gain exposure to a differentiated industrial technology company, aiming to capture durable content growth within vehicles while keeping position size measured. We added H&R Block as a cash-generative, more defensive business to help balance the cyclicality elsewhere in FUND’s portfolio.

We also sold several positions in 2025. We fully exited Seabridge Gold Inc., Radius Recycling, Inc. (following the announcement of its acquisition by Toyota Tsusho America, Inc., a U.S. subsidiary of Toyota Tsusho Corporation), and Gemfields Group Limited, simplifying the portfolio and moving capital away from smaller, more idiosyncratic exposures. Importantly, what may appear to be a new position in OR Royalties Inc. should be viewed as a continuation of existing exposure, since the 2024 holdings list reflects Osisko Gold Royalties Ltd., which rebranded as OR Royalties in 2025.

Finally, the most meaningful resizing among long-term holdings was our increased position in ASA Gold and Precious Metals Limited, and Cal-Maine Foods, Inc., while trimming some of our precious metals mining companies, given their strong performance.

Performance Contributors and Detractors

Figure 4 shows which positions contributed and detracted the most from FUND’s aggregate performance for the 12 months ended December 31, 2025.

Figure 4

Top Contributors to Performance

Year-to-date through 12/31/2025 (%)1

| ASA Gold and Precious Metals Limited | 4.48 |

| Agnico Eagle Mines Limited | 3.90 |

| OR Royalties Inc. | 2.71 |

| Major Drilling Group International Inc. | 2.61 |

| Pan American Silver Corp. | 2.48 |

1 Includes dividends

Top Detractors from Performance

Year-to-date through 12/31/2025 (%)1

| Westlake Corporation | -1.87 |

| FRP Holdings, Inc. | -1.00 |

| Marcus & Millichap, Inc. | -0.85 |

| Cal-Maine Foods, Inc. | -0.45 |

| Helmerich & Payne, Inc. | -0.36 |

1 Net of dividends

Top Contributors to Performance

As shown in Figure 4, ASA Gold and Precious Metals Limited (a closed-end fund that seeks long-term capital appreciation primarily through investing in companies engaged in the exploration for, development of projects or mining of precious metals and minerals) was the largest contributor to performance in 2025, adding 4.48% to FUND’s overall returns, with a total return of 195.6%. Performance accelerated meaningfully in the second half of the year as precious metals prices rose amid heightened global macroeconomic uncertainty. FUND’s exposure to gold and other precious metals proved particularly helpful to performance, while its bias toward small- and mid‑capitalization companies amplified returns, as these businesses tend to exhibit greater sensitivity to rising precious metals prices.

Shares of Agnico Eagle Mines Limited, a Canadian-based gold producer with operations in Canada, Australia, Finland and Mexico, returned 119.5% in 2025 and contributed 3.90% to FUND’s performance. In 2025, Agnico’s shares were supported by consistent execution and a strong cash flow backdrop: the company reported record adjusted net income in Q3 2025 alongside $1.19 billion of free cash flow, and it further strengthened its balance sheet to a $2.16 billion net cash position following meaningful debt repayments. Management also reiterated full-year 2025 guidance of 3.3 to 3.5 million ounces and continued advancing key value drivers, including the Odyssey underground build at Canadian Malartic, Detour Lake’s underground ramp and the Marban project acquired in March 2025 as part of its Canadian Malartic “fill the mill” strategy. Capital returns added support, including an expanded normal course issuer bid authorization of up to $1 billion. Notably, Agnico was also a contributor in 2024, with its share price rising 46.0% and adding 1.87% to FUND’s results.

OR Royalties Inc. was a top-five contributor in 2025 and added 2.71% to FUND’s performance for the year, a benefit of its total return increasing 96.9%. OR Royalties is a precious metals royalty and streaming company that acquires and manages royalties and streams, primarily in Tier 1 jurisdictions, with a portfolio of more than 195 interests anchored by a cornerstone royalty on Agnico Eagle’s Canadian Malartic Complex. OR Royalties shares benefited from strong operating momentum and capital returns, highlighted by the company’s record 2025 royalty and stream revenue of $277.4 million, delivery of 80,775 GEOs (gold equivalent ounces) within guidance, very high cash margins, meaningful share repurchases and a strengthened balance sheet with its credit facility fully repaid and undrawn at year-end. Looking ahead, management’s five-year outlook calls for 110,000 to 125,000 GEOs in 2029, supported by development and expansion catalysts across key assets and partners.

Major Drilling Group International Inc. returned 64.8% in 2025, and the holding contributed 2.61% to FUND’s performance. Major Drilling is the world’s leading provider of specialized contract drilling services for mining and mineral exploration, operating a global fleet of 700-plus drill rigs across multiple continents. Major Drilling’s shares benefited from improving fundamentals through 2025, including management’s December update showing record quarterly revenue of C$244.1 million (up 29% year-over-year), a return to net cash and a normal course issuer bid authorizing repurchases of up to 5% of shares, all signaling confidence and strengthening per share economics. Management also pointed to a constructive 2026 setup as senior miners finalize budgets, supported by higher commodity prices, increased junior financings and growing demand for specialized drilling as new deposits become harder to access. Notably, Major Drilling was a detractor in 2024 (its share price fell 18.2% and it posted a -0.81% contribution to FUND’s results), underscoring the magnitude of the 2025 rebound.

Rounding out the top-five contributors, Pan American Silver Corp. returned 160.3% in 2025 and contributed 2.48% to FUND’s performance. Pan American is a leading precious metals producer, operating silver and gold mines across the Americas and holding a 44% joint venture interest in the Juanicipio mine in Mexico. The company’s shares benefited from a clear step up in cash generation and capital returns, highlighted by record attributable free cash flow of $251.7 million in Q3 2025 and a dividend increase to $0.14 per share, alongside a tighter cost outlook as Juanicipio began contributing. The company also completed the acquisition of MAG Silver Corp. on September 4, 2025, adding Juanicipio and strengthening reserves and expected cash flow, a transaction we view as positively enhancing Pan American’s silver leverage. Operational momentum remained strong into year-end, with 2025 attributable silver production of 22.8 million ounces exceeding updated guidance and a record 7.3 million ounces in Q4, supporting a robust liquidity position and constructive 2026 guidance.

Top Detractors from Performance

Westlake Corporation was the biggest detractor from FUND’s performance in 2025, accounting for 1.87% of the decline as its shares fell 33.8% (net dividends). Westlake is a global manufacturer of petrochemicals, polymers and building products, with meaningful exposure to chlorovinyls and chlor-alkali materials alongside housing and infrastructure products. Shares weakened as pricing and margins compressed amid softer industrial demand, and the company recorded a $727 million non-cash goodwill impairment in its North American chlorovinyls business. In its Q3 2025 update, Westlake management noted that its Housing and Infrastructure Products results were relatively resilient, but Performance and Essential Materials remained pressured, including lower PVC (polyvinyl chloride) resin pricing and a tougher mix toward export volumes. Looking into 2026, Westlake expects margins to benefit from improved plant reliability, $200 million of cost savings and footprint optimization, including closures announced in December 2025 across certain PVC, VCM (vinyl chloride monomer), chlor-alkali and styrene assets as the company responds to industry overcapacity and works to improve profitability and cash generation.

FRP Holdings, Inc. was a top-five detractor in 2025, reducing FUND’s performance by 1.00% as its share price fell 25.6%. FRP is a real estate investment and development company with operations spanning multi-family housing, industrial and commercial properties, a development pipeline and mining and royalty lands. FRP’s stock was pressured as the company reported weaker near-term financial results, including a 51% year-over-year decline in net income that management attributed largely to Altman Logistics Properties, LLC acquisition-related expenses, while pro rata net operating income declined 16% on a difficult comparison versus a prior year one-time $1.9 million catch-up mining royalty payment and softer industrial performance from vacancies tied to an eviction and lease expirations. In sum, 2025 was a foundation-building period for FRP, with a focus on leasing and occupying industrial vacancies and advancing its multi-year development pipeline across Maryland, Florida and South Carolina.

Marcus & Millichap, Inc. reduced FUND’s performance by 0.85% in 2025, with its total return declining 27.6%. Marcus & Millichap is a commercial real estate services firm specializing in investment sales brokerage and providing financing, research and advisory services. Company shares were pressured by price discovery, and Q3 2025 results included a $0.08 per share litigation accrual. However, in Marcus & Millichap’s November 2025 earnings release, Q3 revenue rose 15.1% year-over-year, and management cited a strong pipeline and near-record exclusive inventory. Management also said a more accommodative Federal Reserve stance should support improving trading volumes, even if the 10-year Treasury yield has been less responsive than a year ago. With about $59 million of repurchase capacity remaining, Marcus & Millichap has the flexibility to repurchase shares while the transaction market normalizes.

Cal-Maine Foods, Inc. was the fourth-largest detractor in 2025, reducing FUND’s performance by 0.45% as its total return declined 15.6%. In 2024, however, Cal-Maine was a top contributor, adding 2.37% to portfolio performance, as it returned 87.1%. Cal-Maine is the largest egg company in the United States, producing and distributing shell eggs, as well as a growing range of egg products and prepared breakfast foods. After its 2024 windfall, Cal-Maine results cooled as egg markets normalized and year-over-year selling prices fell sharply, pressuring earnings. Management is investing to diversify revenues, with specialty eggs and prepared foods accounting for 46.4% of net sales, a $36 million prepared foods expansion and the Clean Egg, LLC asset purchase to grow specialty and free-range supply. The June 2025 Echo Lake Foods acquisition broadened Cal-Maine’s prepared foods platform, while the April 2025 conversion of super voting shares ended controlled company status and coincided with a $500 million repurchase authorization. Overall, 2025 was an eventful year for Cal-Maine and its long-term prospects look strong.

Finally, Helmerich & Payne, Inc. ranked as the number five detractor, impacting FUND’s results by -0.36% as its total return declined 6.2%. Helmerich & Payne is a leading drilling contractor that designs, fabricates and operates high-performance drilling rigs and provides technological solutions, including automation and directional drilling. In 2025, the company’s shares were weighed down by a more cautious U.S. land-drilling backdrop and integration-related noise following Helmerich & Payne’s $1.97 billion acquisition of KCA Deutag International Limited, which broadened its global footprint but increased near-term complexity and costs. In its fiscal 2025 reporting, Helmerich & Payne posted a consolidated net loss and highlighted non-recurring items, while North America Solutions continued to deliver market-leading direct margins even as International Solutions remained challenged. Looking ahead, management’s initial fiscal 2026 outlook emphasized lower capital spending, accelerated debt reduction and improving international activity, including notices to reactivate seven rigs in Saudi Arabia during the first half of 2026. Helmerich & Payne also announced an orderly CEO transition with Trey Adams set to succeed John Lindsay after the March 2026 annual meeting.

Outlook

For 2026, we expect more of the same volatility experienced in 2025. There will be more turbulence on the world stage as geopolitical conflicts continue with some new adventures in Venezuela and Greenland thrown into the mix.

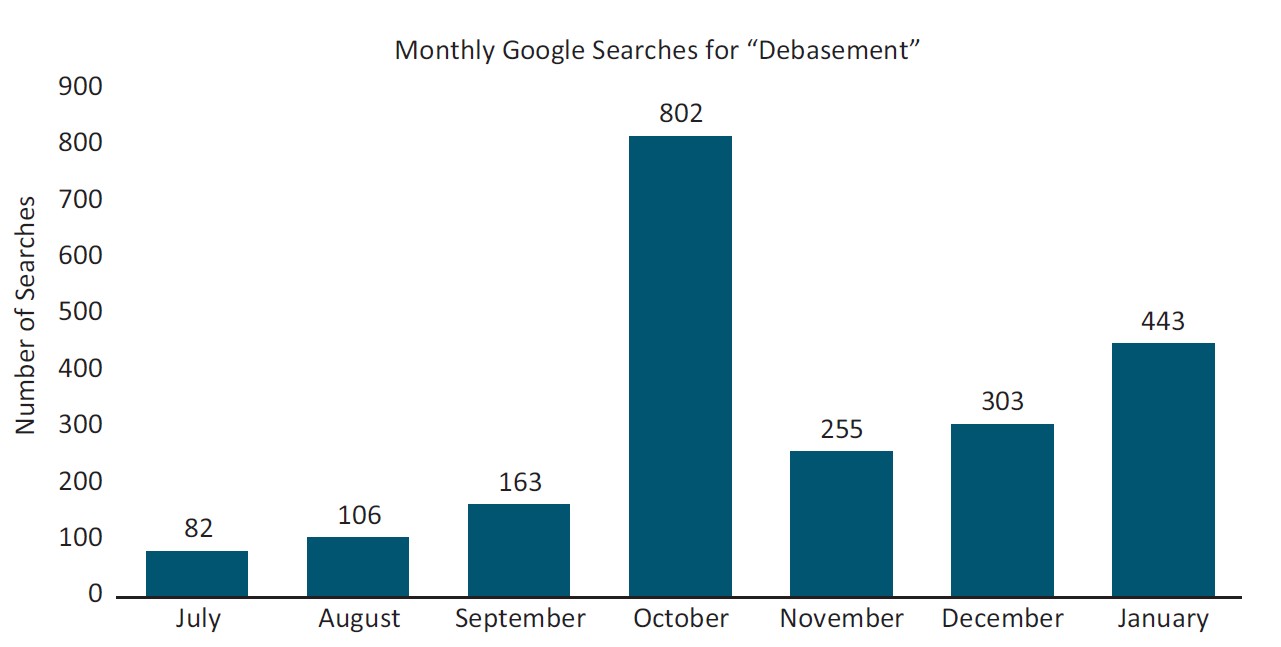

We recently experienced a swift and violent selloff in precious metals following an exceptional run for gold and silver prices. In our view, this is a healthy and overdue technical correction triggered by speculative investors and algorithmic traders while the fundamental drivers of the rally remain intact. Chief among these trends is what has become known as the “Debasement Trade”. The Debasement Trade reflects a structural regime in which fiat currencies gradually lose purchasing power as persistent fiscal deficits, debt monetization and ongoing liquidity injections erode real value over time. A little-known concept just a year ago, the term has now entered the mainstream vernacular. Google searches for “debasement” and “dollar debasement” started rising last summer when the Trump administration began escalating its threats on the independence of the Federal Reserve. Search activity peaked in October 2025 with “debasement” officially becoming a trending term. Searches are once again on the rise in early 2026.

The Debasement Trade was a major feature coming into 2026 as investors of all classes reviewed their portfolio allocations and positioning. Given the Trump administration’s aggressive negotiating tactics and foreign policy, we should expect more “S.A.D.” (Sell America Down) in the global investment community. Further, we are in an election year with consumer affordability the number-one issue. Since losing political ground on this problem last November, the Trump administration has started making populist proposals that would please the most aggressive progressives. Caps on credit card interest, bans on institutional investments in single-family homes and taxpayer-funded $1,000 grants to newborns’ accounts are all ideas likely to backfire. The U.S. Treasury is now buying back tens of billions of its own paper each month, and instructions have been given to the Fannie Mae and Freddie Mac agencies to buy back $200 billion of mortgages. Clearly, while this is not called Q.E. (quantitative easing), money printing is back and its long-term inflationary effects will do nothing to improve affordability.

We remain optimistic that FUND is well-positioned to weather the fiscal and geopolitical storms ahead. We have been early in our hard asset exposures, but the world is waking up to the fact that you can’t have digital without underlying physical assets and the power to run them.

As always, we thank all our colleagues at Sprott who help us manage FUND smoothly and efficiently. Ryan McIntyre has become a valuable partner in not only FUND’s management, but as a newly appointed President of Sprott Inc. Basia Dworak continues to run our lives and has become a Managing Partner at Sprott Inc. Congratulations to both Ryan and Basia. Finally, thank you to all our patient shareholders for your trust. Please call us if you have questions or just want to check in, 203.656.2430.

Sincerely,

W. Whitney George,

Senior Portfolio Manager

The views expressed above reflect those of Mr. George as of the date stated above and do not necessarily represent the views of Sprott Asset Management USA, Inc. or any other person in the Sprott organization. Any such views are subject to change at any time based upon market or other conditions and Sprott disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for the Sprott Focus Trust are based on numerous factors, may not be relied on as an indication of trading intent on behalf of the Sprott Focus Trust.