For the latest standardized performance and holdings of the Sprott Lithium Miners ETF, please visit LITP. Past performance is no guarantee of future results.

Key Takeaways

- Lithium’s Market Has Rebounded Sharply: After a steep correction following the 2022 price spike, lithium prices have staged a strong recovery, rising more than 125% over the past 12 months.

- Lithium Is Becoming a Strategic Commodity: Policies such as the U.S. Section 232 critical minerals review, international supply agreements and strategic reserves are introducing incentives that could influence investment and pricing.

- Policy Is Reshaping Supply Chains and Financing: Critical minerals alliances, including the U.S.-Argentina framework, aim to accelerate project development, while initiatives like Project Vault signal a shift toward government-backed stockpiling and greater public-sector involvement.

- Supply Risks Are Increasingly Policy Driven: Disruptions in Zimbabwe and China highlight the fragility of lithium supply and the growing influence of geopolitical factors on prices.

- Energy Storage Is Emerging as a Major Demand Driver: Battery energy storage is becoming a second pillar of lithium demand alongside EVs, driven by AI, data centers and rising global investment in storage.

Performance as of February 28, 2026

| 1 MO* | 3 MO* | YTD* | 1 YR | 3 YR | 5 YR | |

| Lithium Spot Price1 | 5.33% | 77.61% | 35.63% | 125.65% | -24.38% | 13.06% |

| Lithium Mining Equities (Nasdaq Sprott Lithium Miners Index TR)2 | 6.75% | 24.47% | 16.65% | 149.11% | -2.80% | 11.12% |

| Broad Commodities (BCOM Index)3 | 0.81% | 10.21% | 10.93% | 18.43% | 4.65% | 7.37% |

| U.S. Equities (S&P 500 TR Index) 4 | -0.76% | 0.74% | 0.68% | 16.99% | 21.80% | 14.19% |

High short-term performance, when observed, is unusual and investors should not expect such performance to continue or be repeated. Performance for periods of less than one year are not annualized. Source: Bloomberg as of 02/28/2026. You cannot invest directly in an index. Past performance is no guarantee of future results.

Performance Overview: The Lithium Rebound

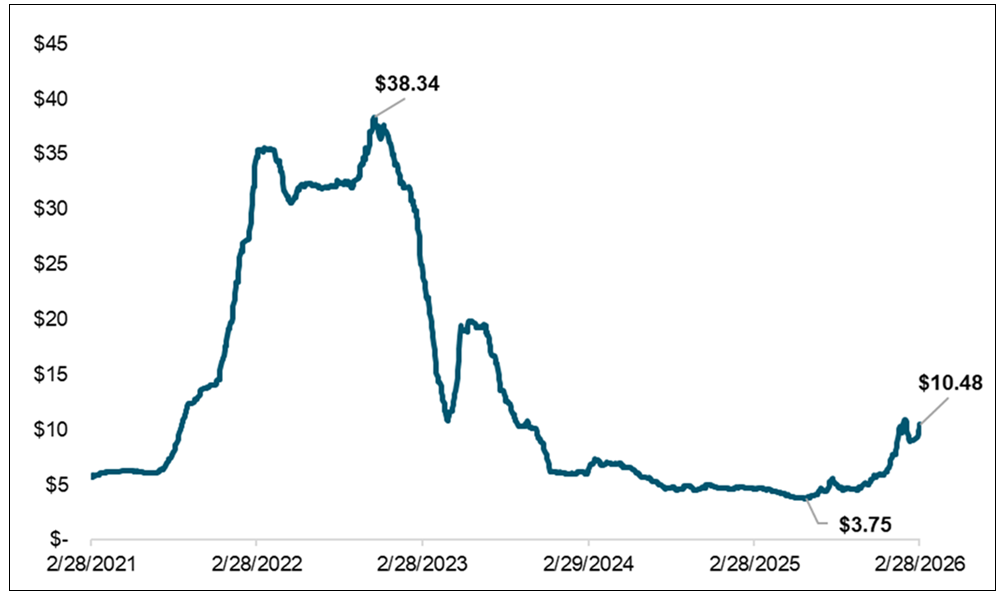

Lithium is in the spotlight given its strong performance over the past year, with the spot price gaining 35.63% year-to-date as of February 28, 2026, and rising 125.65% over the past 12 months. Lithium has entered a new phase where the market is no longer trading on a simple surplus narrative.

After one of the most volatile boom-bust cycles in modern commodities, lithium’s price behavior is increasingly shaped by demand broadening beyond electric vehicles (EVs), led by rapid growth in stationary storage, while the reliability of marginal supply is becoming more policy-sensitive. At the same time, governments are treating critical minerals less as inputs and more as strategic assets, with trade actions and stockpiling initiatives introducing a new layer of optionality that can influence incentives, investment and ultimately the price.

Lithium gets its ‘white gold’ moniker because it is a highly valuable, silvery-white metal essential for the energy transition.

The past several years have underscored that lithium is not a mature commodity market. The cycle began with a dramatic upswing in 2021 as prices rose from roughly $5 per pound, culminating in a peak of $38.34 per pound in November 2022, levels described by many industry participants as extreme and unsustainable (see Figure 1). A wave of supply growth followed, and as the market was flooded with new production, lithium prices fell sharply through to mid-2025. By June 2025, lithium had reached a low, and the market began to stabilize, setting the stage for a rebound that has since attracted renewed investor attention.

Prices have reacted sharply to incremental changes in perceived supply reliability and near-term demand momentum, particularly in China. The lithium spot price jumped 180% between June 23, 2025, and February 28, 2026, reaching $10.48 per pound, levels not seen since 2023.

Three themes help explain why the lithium market has become so responsive. First, demand growth is becoming more diversified. Energy storage systems are emerging as a fast-growing second pillar of battery demand, potentially tightening the market faster than expected. Second, supply is proving more sensitive to regulatory and permitting outcomes than the surplus narrative implies. In China, permit cleanups and uncertainty around mine resumptions have become bellwethers of market psychology. Third, the strategic bid is rising. The United States has explicitly framed processed critical minerals as a national security issue under Section 232, while broader stockpiling initiatives and the concept of a lithium strategic reserve are increasingly part of the policy discourse.

Figure 1. Lithium Spot Price Regains Momentum (2/28/2021-2/28/2026)

Source: Bloomberg and Sprott Asset Management. Data as of 02/28/2026. The Lithium Spot Price is measured by the L4CNMJGO Index. The definition of this index is provided in the footnotes. You cannot invest directly in an index. Past performance is no guarantee of future results.

Three Market Drivers that Aren’t EVs

The Strategic Bid for Lithium

Policy actions are creating a market environment in which reliable lithium supply is actively prioritized, improving confidence and capital availability for lithium producers. This shift is showing up through several reinforcing channels: a growing web of critical minerals agreements and alliances aimed at securing supply, an increased willingness in the U.S. to use trade policy to support domestic production (including the potential of price floors and tariffs), the expansion of stockpiling and strategic reserve frameworks to cushion supply shocks and volatility, and more direct government participation in project financing, including direct equity stakes.

As lithium becomes a national security priority, policy is beginning to reshape the economics of the market.

First and foremost, the U.S. has initiated a Section 2325 action focused on critical minerals, including lithium, concluding that reliance on imports poses a threat to national security.6 That finding reframes lithium as an input the U.S. needs to secure, not simply source. Further, it sets out a clear response pathway. It directs the U.S. to negotiate with trading partners to adjust critical minerals supply relationships and reduce exposure to vulnerable supply chains. The language is especially notable because it links national security objectives to mechanisms that can influence market outcomes, including the prospect of price floors, signaling that policymakers are now thinking about what keeps supply chains investable and financeable over time.

Building Supply Chain Alliances: U.S.-Argentina Critical Minerals Framework

This negotiation-first approach matters because it ties the strategic bid directly to a new wave of critical minerals agreements. Instead of relying solely on domestic policy, the U.S. is signaling its intent to secure supply through formal frameworks with resource-rich partners. A timely example is the U.S.-Argentina critical minerals framework announced in early February 2026, linking the United States with the world’s fifth-largest lithium producer.7

Supply security for lithium and other critical minerals is being negotiated between nations.

The agreement is stated to strengthen critical minerals supply chains and accelerate secure, diversified supply, with governments and the private sector mobilizing support through grants, guarantees, loans and equity investments, while also leveraging U.S. demand and strategic stockpiling alongside Argentina’s investment incentive regime, RIGI Régimen de Incentivo para Grandes Inversiones)8. Further, it commits “to jointly identifying priority projects and facilitating their financing within six months, creating a sustainable long-term partnership based on fair market pricing.”9 Clearly, critical minerals agreements may expand financing availability for the capital-intensive mining industry.

We believe that further developments between critical minerals-producing countries and developed countries, not just the U.S., may ultimately be beneficial for lithium producers, providing a supportive financing path from resource to production.

If negotiated frameworks do not achieve the intended outcomes, Section 232 keeps additional levers on the table that could further reinforce investment conditions for the lithium market. The explicit reference to price floors is important because it points to policy tools that can reduce the downside damage of commodity cycles (see Figure 1 above, which showcases lithium volatility) by supporting a more durable economic backdrop for strategically important supply chains. While the exact design of any lithium-specific price floor has not been laid out, similar thinking has already been proposed for other critical minerals. For example, in July 2025, the U.S. Department of Defense struck a long-term agreement with rare earths producer MP Materials that included a 10-year price floor set well above prevailing market prices at the time, alongside long-term offtake commitments and a major equity investment, illustrating how price support can be used to de-risk domestic supply chain buildouts.10

Finally, Section 232 preserves the possibility of lithium tariffs as a distinct mechanism if negotiations fail. That is worth separating from the country-specific tariffs that the Supreme Court recently struck down. Section 232 has its own trade authority and is framed as a national security tool focused on critical minerals. For example, the possibility of a 50% Section 232 tariff on copper last year had profound implications on the market by increasing the U.S. copper price to a 30% premium over the LME (London Metal Exchange, used as an international benchmark) and resulting in large imports of physical copper into the U.S. in anticipation of the premium.

Project Vault Launches in February 2026

Policy is also moving beyond trade tools and into buffering mechanisms, with governments increasingly treating critical minerals as inputs that require backstops, not just supply chains. In early February 2026, “Project Vault” was announced, which is a planned U.S. strategic stockpile of critical minerals with $12 billion in seed funding, structured as $1.67 billion in private capital plus a $10 billion loan from the U.S. Export-Import Bank, designed to procure and store critical minerals.11

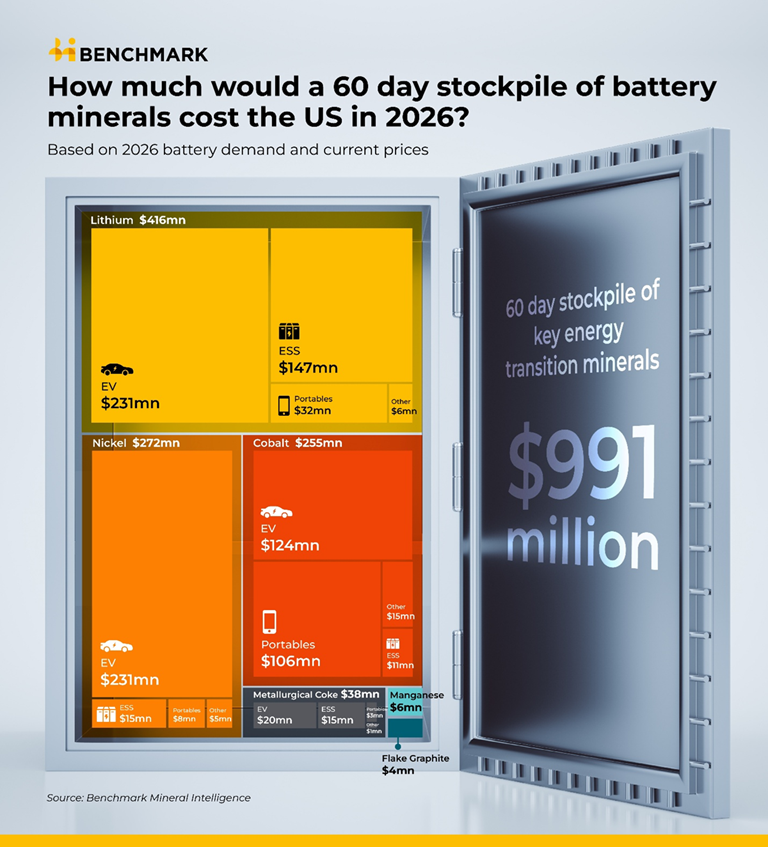

Project Vault aims to create a strategic buffer of critical materials, releasing physical inventories during supply disruptions and assuring domestic industries that emergency reserves are held within U.S. borders, similar to the Strategic Petroleum Reserve. The aim is to build strategic stocks equivalent to 60 days of demand for selected minerals, including lithium. At today’s prices and based on 2026 demand, Benchmark Minerals estimates this would cost $991 million for key battery minerals (lithium, cobalt, nickel, manganese, graphite and coke), with lithium as the largest contributor at $416 million (see Figure 3).

Project Vault underscores that reliable critical minerals supply is now a national security priority.

Importantly, Project Vault reflects a broader global trend: Governments are moving to build or expand strategic buffers of critical minerals as these materials become increasingly tied to national security. In January 2026, Australia committed $1.2 billion to establish a Critical Minerals Strategic Reserve, with operations expected to begin in the second half of 2026. China has also reportedly been adding to its strategic reserves of metals, including lithium, underscoring that major economies across the supply chain increasingly view stockpiles as a strategic lever.

For lithium markets, the relevance is twofold. First, stockpiling is explicitly intended to support resilience during disruptions by ensuring some emergency supply is available and by reducing the risk of sudden shortages cascading into shutdowns. Second, these programs can reinforce the idea that the reliability of critical minerals supply is a priority, thereby supporting confidence and investment conditions across the industry during volatile periods.

Figure 2. U.S. Government Supports Lithium Americas’ Thacker Pass Project

Source: Lithium Americas is building an industrial-scale battery-grade lithium carbonate production capacity at Thacker Pass, Nevada.

Finally, the strategic bid does not stop at holding inventory. The strongest proof that this strategic bid is moving from concepts to balance sheets is the example of Lithium Americas Corp.12 The U.S. Department of Energy explicitly restructured its support for the company in a way that gives the U.S. government a direct, equity-linked interest in a lithium miner and its flagship project, describing the change as a step to strengthen loan resilience, better protect taxpayers and help solidify the launch of a domestic source of lithium carbonate.

Lithium is becoming less of a purely cyclical commodity and more a strategic commodity shaped by policy.

The Department of Energy (DOE) also framed the move as advancing onshoring priorities and securing access to a strategically important deposit, making clear that this is not just a financing package but an economic-security decision with explicit supply-chain intent. This followed an equity investment by GM and ultimately provides a concrete example of improved funding conditions for producers positioned to deliver a reliable supply of lithium.

Taken together, these developments suggest that lithium is becoming less of a purely cyclical commodity and more a strategic commodity shaped by policy. Section 232 introduces a pathway that can affect incentives; Project Vault introduces the potential for buffer inventories to reduce shock-driven behavior; and the Lithium Americas structure demonstrates that strategic objectives can translate into specific funding. Ultimately, we believe that all of these developments put lithium miners in a better position than current pricing suggests.

Figure 3.

Source: https://source.benchmarkminerals.com/article/how-much-would-60-days-of-us-battery-minerals-cost-in-2026-

Zimbabwe and China Disruptions Highlight Lithium’s Supply Fragility

The most consequential recent development in lithium supply is Zimbabwe’s abrupt suspension of exports, which removes a meaningful swing source of lithium feedstock to China at a time when the market is already highly sensitive to policy risk. On February 25, Zimbabwe announced an immediate halt to exports of lithium concentrates and raw minerals, stating that the measure would remain in place until further notice.13 The government framed the move as being in the national interest, linking it to efforts to tighten oversight of the sector and accelerate domestic value addition so that more economic benefit is retained within the country.

Part of a broader pattern of national policies shaping supply across critical minerals.

The decision also represents a significant timeline shock. Zimbabwe had previously signaled that such restrictions would take effect in 2027, so the immediate suspension effectively moves the policy clock forward. The move comes amid a broader fiscal push to force beneficiation (e.g., turning lithium ore or concentrate into refined lithium chemicals). Beginning January 1, 2026, Zimbabwe implemented a 10% VAT (Value-Added Tax) on lithium ore exports, explicitly designed to encourage domestic processing rather than the shipment of raw material.14

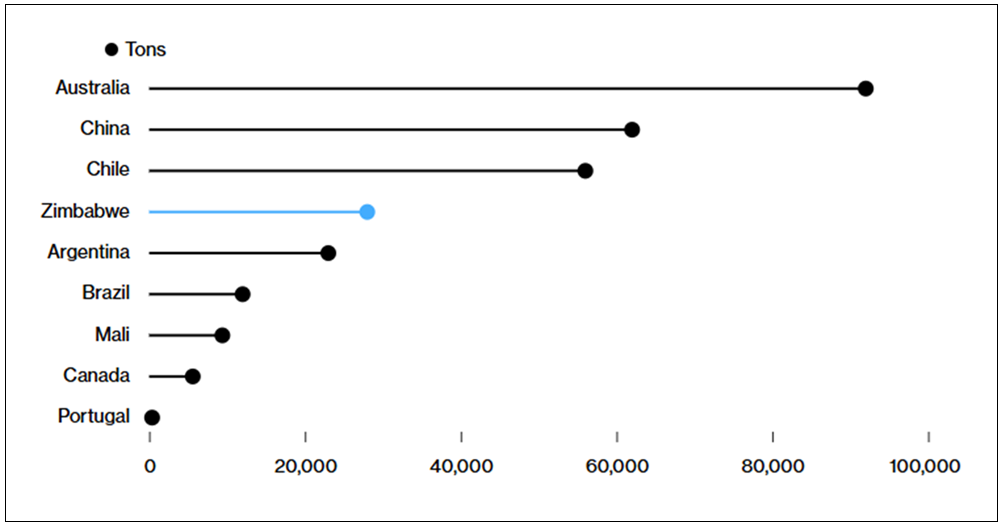

Zimbabwe is far from a marginal supplier. It produced roughly 10% of global mined lithium last year and ranks as the fourth-largest producer worldwide, making any disruption there immediately price-relevant (see Figure 4).

Stepping back, Zimbabwe’s move follows a familiar playbook, with Indonesia’s nickel market providing the clearest precedent. By banning exports of nickel ore and concentrates, Indonesia forced investment into domestic processing and downstream capacity. This policy ultimately pushed the country up the value chain, driving higher-value exports, expanded downstream production and increased foreign investment linked to in-country processing.

We see this as part of a broader pattern of national policies shaping supply across critical minerals. The DRC’s (Democratic Republic of the Congo’s) cobalt policy has repeatedly used export controls as a market lever, including a 2025 export ban. Guinea’s bauxite strategy has similarly leaned on regulatory pressure to accelerate local refining.

The takeaway for the lithium market is that the “rules of supply” are increasingly shaped by policy decisions, which is why markets can reprice quickly when a top supplier tightens export rules without a transition period.

Figure 4. Zimbabwe and China Lithium 2025 Supply Was Significant

Source: Bloomberg and U.S. Geological Survey, Mineral Commodity Summaries, February 2026.

The next major swing factor is China, specifically CATL’s (Contemporary Amperex Technology Co. Limited’s) Jianxiawo lithium mine, where regulatory enforcement intersects with high-cost supply. Mining has been suspended since early August, following the site’s license expiration, with CATL working to renew it. The mine accounts for roughly 3% of global lithium output, helping explain why prices have reacted to headlines around its suspension and restart timeline. A restart had been widely expected shortly after the Chinese New Year, but that window now appears to be slipping. A first-quarter restart looks increasingly unlikely amid reports of remediation tied to tailings pond impermeability and the mine’s proximity to a nearby river system, with approvals and timelines still uncertain.

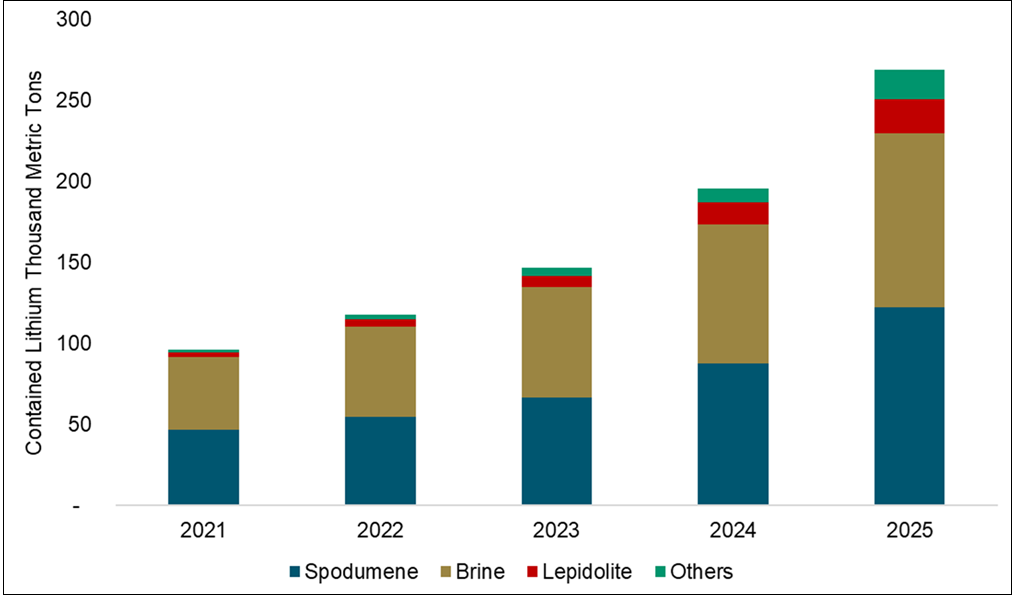

The disruption is amplified by both the operator and the type of supply. CATL is the world’s largest battery manufacturer, with about 39.2% global market share in 2025. Further, this disruption is occurring at a lepidolite operation. Lepidolite is materially more expensive due to its lower lithium grade and more complex extraction process, and can become uneconomic quickly. In China, lepidolite-based supply expanded rapidly during the 2021–2022 price spike as producers chased margins, and that incremental tonnage ultimately contributed to the market's oversupply as prices normalized (see Figure 5). Even after profitability was squeezed, lepidolite supply has been growing because a meaningful portion of China’s system is vertically integrated, like CATL, and integrated players have been able to keep high-cost units running while capturing economics further downstream, prolonging supply and weighing on the market’s rebalancing.

Now this dynamic may be changing. China has announced a 2025-2026 "anti-involution" campaign targeting overcapacity in sectors like lithium mining to end destructive pricing and improve profitability. Evidently, the extended suspension of the world's largest battery manufacturer's low-yielding and large lithium mine has been a supportive and price-stabilizing development for the lithium market. The restart timeline of this mine will be important to watch, as will the timelines of other Chinese mines facing similar hurdles.

Ultimately, we believe the disruptions in China and Zimbabwe are elevating lithium’s supply risk profile, increasing the likelihood of a higher security premium. This dynamic could bring the market into balance—and potentially deficit—earlier than current forecasts suggest.

Figure 5. The Rise of Lepidolite: Lithium Supply by Resource Type

Source: BloombergNEF. Data as of 06/18/2025.

Energy Storage Demand Becomes the Swing Factor

Energy storage is increasingly becoming the swing factor in battery demand, and the scale of growth is now large enough to shift the lithium market balance on its own. Battery energy storage demand grew 51% in 2025,15, well ahead of roughly 29% growth across total lithium-ion battery demand, lifting storage to about a fifth of total global battery demand. This shift in storage demand is increasingly driven by grid reliability and power-market dynamics.

Texas is set to overtake California in 2026 as the largest energy storage market in the U.S.

The U.S. is a good example of how quickly this demand channel is scaling. The U.S. energy storage industry installed a record 57.6 GWh of new capacity in 2025, the largest single-year addition of battery capacity on record.16 Installations rose 30% from the previous record in 2024 and were four times what the industry installed just three years ago. This growth has not been confined to traditional clean-energy strongholds. Two-thirds of all utility-scale energy storage capacity installed in 2025 was built in states won by President Trump in the 2024 election, including nine of the top 15 states for new installations. Texas is set to overtake California as the largest energy storage market in the country in 2026. This is a useful proof point that storage deployment is being pulled by reliability and economics, not only policy branding.

China underscores the magnitude of what is developing globally. 65 GWh of grid-scale battery energy storage entered operation in China in December 2025 alone, exceeding the total installed in the U.S. for all of 2025.17 December is often the biggest month for new capacity as developers race to meet installation commitments and calendar-year capex deadlines. Benchmark notes that China’s December figure accounted for about 41% of its annual installed capacity, up sharply from about 25% in 2024. The roughly 65 GWh installed in December also represented a ~135% year-on-year increase. Taken together, the U.S. and China examples show storage is not just growing, it is compounding at a pace that can tighten lithium balances when supply is constrained.

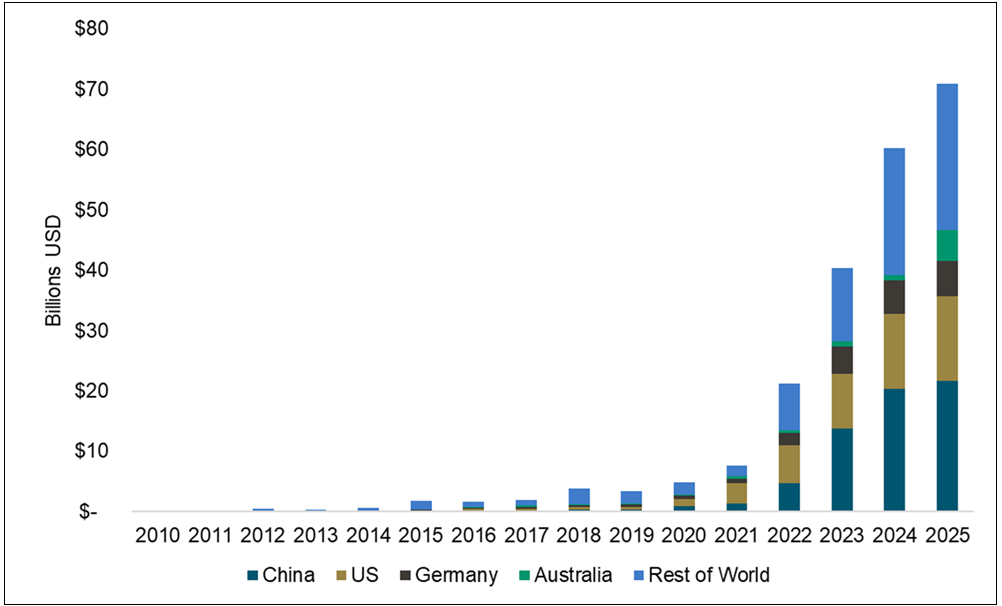

This demand channel is also being reinforced by investment. $71B was invested in energy storage projects globally in 2025 across utility-scale, commercial and residential segments, a new record that was 18% higher than 2024 (see Figure 5). This investment was also fueled by a sharp decline in turnkey battery storage system costs in 2025, with the volume-weighted average cost falling 31% to $117/kWh, which supported scaling. Storage investment was broad-based by region, led by Asia Pacific and followed by EMEA (Europe, Middle East and Africa) and the Americas, with utility-scale projects accounting for the majority of total investment.

Lithium demand is undergoing a structural shift. Energy storage is no longer just "incremental" and is now scaling rapidly enough to tighten global balances, even without a broader market surge.

- The AI Factor: Data center growth is accelerating the buildout as grids seek the flexibility to handle massive new loads.

- The Shift: Price support has moved beyond the EV market. It is now driven by a "triple threat" of grid investment, reliability upgrades and energy security.

Figure 6. Investment in Energy Storage Hits Record High in 2025

Source: BloombergNEF. Data as of 01/26/2026. Included for illustrative purposes only.

Lithium Enters a Policy-Driven Era of Supply Security and Strategic Demand

Going forward, lithium markets will be increasingly shaped by policy decisions rather than solely by market dynamics. First, watch the evolution of critical minerals agreements and trade negotiations, particularly the U.S. Section 232 process covering processed critical materials. The presidential proclamation frames critical minerals as a national security issue and opens the door to price floors, tariffs and negotiated import frameworks if talks fail to deliver results. These mechanisms could become explicit policy price signals designed to incentivize new supply.

Lithium has moved from an EV story to a strategic infrastructure asset.

Second, stockpiling is moving from concept to implementation. The U.S. has launched Project Vault, a $12 billion public-private initiative to establish a Strategic Critical Minerals Reserve for civilian supply chains. Governments globally, including China, are increasingly building critical minerals inventories as protection against supply shocks and supply-chain fragility.

Third, the pace of permitting reform and financing support for new supply will be critical. The U.S.-Argentina critical minerals framework highlights an emerging policy toolkit: grants, guarantees, loans, and equity investments, paired with streamlined permitting and benchmark pricing frameworks designed to accelerate project development.

Fourth, investors should monitor supply constraints in China and other producing regions. Delays in restarting CATL’s Jianxiawo mine and Zimbabwe’s abrupt lithium export ban illustrate how policy and regulatory decisions can rapidly reshape supply availability.

Finally, energy security dynamics are reinforcing lithium demand through grid storage. Rising power consumption from AI infrastructure and data centers is increasing the importance of energy storage as reliable infrastructure.

Taken together, the investment case for lithium is broadening. Electric vehicles remain a major demand driver, but lithium is increasingly supported by multiple structural forces spanning energy security, grid infrastructure and policy-driven supply chains.

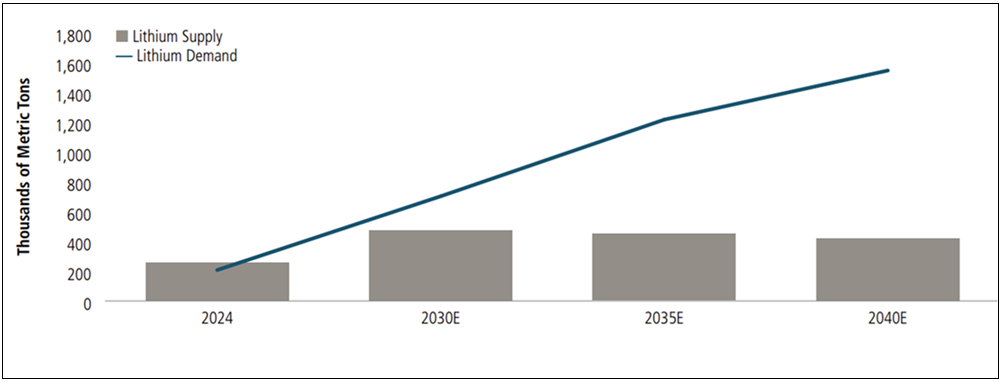

Figure 7. Lithium Supply and Demand Imbalance Likely to Invert

Source: “Global Critical Minerals Outlook 2025”, International Energy Agency (IEA), May 2025.

Footnotes

Important Disclosures

Unless otherwise specified, the reader should assume any companies mentioned are not current holdings of LITP.

An investor should consider the investment objectives, risks, charges, and expenses of each fund carefully before investing. To obtain a fund's Prospectus, which contains this and other information, contact your financial professional, call 1.888.622.1813 or visit SprottETFs.com. Read the Prospectus carefully before investing.

Exchange Traded Funds (ETFs) are considered to have continuous liquidity because they allow for an individual to trade throughout the day, which may indicate higher transaction costs and result in higher taxes when fund shares are held in a taxable account.

Diversification does not protect against loss. The funds are non-diversified and can invest a greater portion of assets in securities of individual issuers, particularly those in the natural resources and/or precious metals industry, which may experience greater price volatility. Relative to other sectors, natural resources and precious metals investments have higher headline risk and are more sensitive to changes in economic data, political or regulatory events, and underlying commodity price fluctuations. Risks related to extraction, storage and liquidity should also be considered.

Shares are not individually redeemable. Investors buy and sell shares of the funds on a secondary market. Only “authorized participants” may trade directly with the fund, typically in blocks of 10,000 shares.

The Sprott Active Metals & Miners ETF is new and has limited operating history.

Sprott Asset Management USA, Inc. is the Investment Adviser to the Sprott ETFs. ALPS Distributors, Inc. is the Distributor for the Sprott ETFs and is a registered broker-dealer and FINRA Member. ALPS Distributors, Inc. is not affiliated with Sprott Asset Management USA, Inc.